Market Commentary

Gold — Getting Ready to Shine Again?

These pages have been in and out of the gold trade since July 22, 2025, when Pinebrook initiated a long position in gold futures. The framework underpinning that trade was laid out a week later, on August 1st, in a note titled Gold — A Demand Story.

The core argument was straightforward: gold’s financialization via the GLD ETF in 2004 had transformed it from a barbarous relic into a fully fungible, 21st-century financial instrument. Central bank accumulation, an insatiable retail bid, and gold’s evolving hybrid risk-on/risk-off correlation profile made it a structurally sound long.

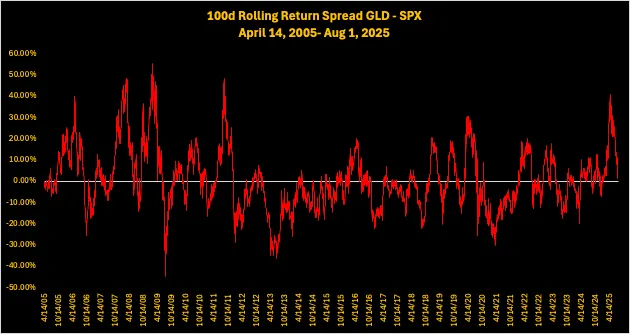

At the time of that August note, the 100-day rolling GLD-SPX spread sat at 5.09%, having compressed sharply from 41.24% at the April 2025 tariff-tantrum peak.

The S&P 500/gold ratio was 1.86x against a long-term average of 1.6x, implying a fair-value gold price of approximately $3,900/oz.

By September 5th, a note titled New Trade Discussion added gold miners for convexity. The rationale: junior miners in the GDXJ ETF were operationally leveraged to the gold cycle, reporting record revenues, record earnings, record operating cash flow, and a record average profit per ounce of $1,900 against all-in sustaining costs. Miners had delivered 70–90% year-over-year earnings growth for eight consecutive quarters. Pinebrook preferred GDXJ over GDX for its superior growth profile.

Then came October 20th. Gold had risen 132% from its October 2, 2023, bull-market birthday, the strongest absolute advance in the history of the yellow metal.

The GLD ETF had closed within a whisker of being 2-standard deviations overbought relative to the S&P 500 on a one-calendar-year lookback, reaching 47.22% versus a 2-sigma threshold of 48.19%.

The same note sounded caution. The average drawdown across the prior gold bull cycles was -16.3%. A correction was less of a matter of if and more of when and how deep.

The answer came on January 28, 2026, when gold peaked at $5,417.21/oz, having surged a parabolic 25.1% in January.

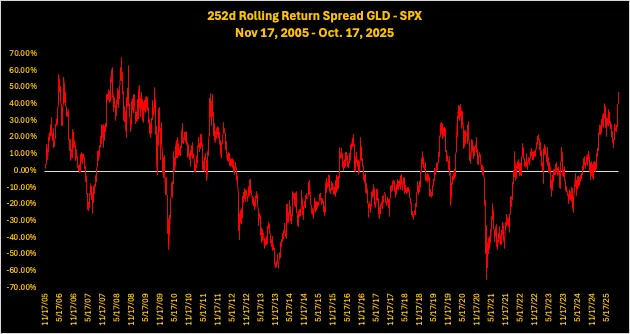

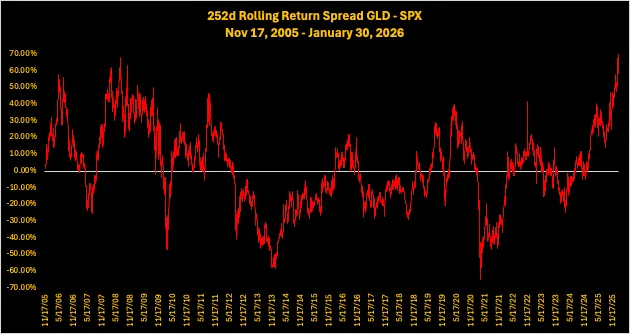

At peak, the GLD/SPX spread was stretched to 79.69% above its 200-day rolling return, the most overbought reading since March 1980.

On a one-year rolling basis, the GLD-SPX rolling return spread was more than 3 standard deviations above the mean, a level unseen in 20 years of data.

In a note titled Miners, published February 2, 2026, Pinebrook got short the miners.

Five Months of Reckoning

Gold’s drawdown from the January 28th peak has been ugly. As of June 11, 2026, gold spot trades at $4,212.26/oz, a decline of 22.24% from the January 28th peak of $5,417.21/oz.

The June 11, 2026, intra-day low of $4024.01/oz. represents a peak-to-trough drawdown of -25.72%, exceeding every prior correction in the post-2006 gold super-cycle, where the historical average peak-to-trough decline across 11 prior episodes was -16.30%.