U.S. Economic Growth Update

Front-Running the Warsh Reaction Function Into H2 2026

Executive Summary

Growth into H2 2026 rests on three pillars: a consumer spending story that is nominally strong but real-income weak; an AI capex cycle that is now visibly bleeding into the physical economy; and a labor market showing the first hard signs of reacceleration after a year of stagnation.

Pinebrook’s focus is on the compositional undercurrents that the headline numbers don’t show, and the Fed’s reaction function to the forward evolution of the data.

Historically, cycles that looked like this — long leading indicators flashing yellow, real income negative, headline data still fine — have been rescued by two things: decelerating producer prices and loose fiscal policy.

June’s jobs report, which was weak on payrolls but strong on unemployment, bought the Fed some time: the rate hike that was getting priced for October has been kicked to December.

Pinebrook’s 10-year short position was closed at a loss — the first rates loss of the year.

The house view on the rates complex is neutral pending clarification from the July jobs report and the August Supercore read.

Where We Left Off

Back in April of this year, we were in phase one of the energy supply shock timeline, when the ceasefire suddenly removed the worst-case tail and concentrated probabilities toward the AI earnings cycle thesis and drove the equity recovery.

Productivity had not collapsed, and labor hoarding kept U3 stable while hours worked and soft survey sentiment deteriorated.

The sectoral sequencing that was laid out — transportation and logistics first, manufacturing second, construction third, consumer goods fourth, services last — had begun its first stage.

The key regime question — temporary price volatility or persistent supply instability — was the unknown.

What was known was that the U.S. was entering the shock from a position of relative strength due to its reserve currency status, energy self-sufficiency, and an AI investment boom standing in for the late-90s tech cycle.

Thus, Pinebrook’s very wrong call for zero GDP growth output was offset by the very correct view that the U.S. comes out ahead of its peers and that the AI capex cycle would hold long enough to bridge the wedge between shock and normalization.

That thesis has aged well.

The Iran MOU was signed on June 17 and closed out the acute phase of the shock.

Brent is back to pre-conflict levels near $72.

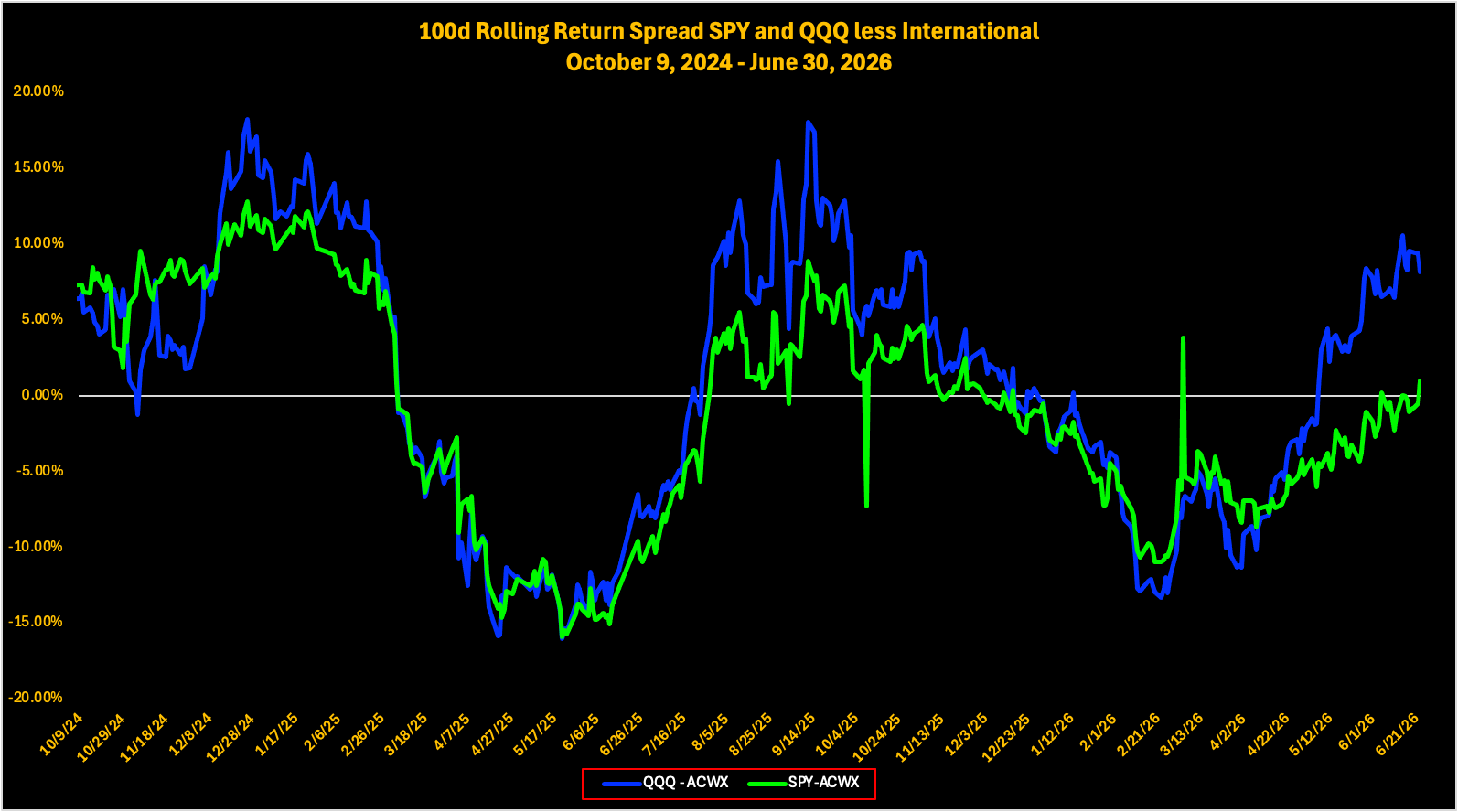

The left-tail growth risk has been shot in the head, and U.S. assets outperformed RoW assets on a 100-day rolling return basis.

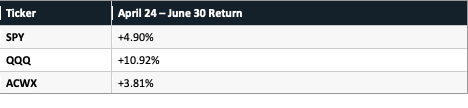

For those watching at home, the math holds the same on an absolute price return basis (April 24 – June 30):

While we got the trade right (what really matters), we got the economics wrong.

The Strait closed in late February; the Iran MOU wasn’t signed until June 17 — roughly three and a half to four months of acute disruption, longer than the one-month kinetic baseline the March 30th note built its GDP math around.

The shock ran longer than assumed, not shorter, and growth still came in near 2.7%.

That means the miss was an underestimate of the offsetting forces — the restocking cycle, labor hoarding, and above all the AI capex cycle — relative to the mechanical GDP drag modeled from the supply shock.

Looking Forward