Market Commentary

Heavy Metal

On January 28, 2026, gold (the physical, with the ticker XAU <Currency>, not a paper contract or ETF) peaked as 5417.21/oz.

Closing March 23, 2026 at 4407.18, this represents a -18.64% corrective move, with -12.19% of that happening over the past week alone.

This is a classic corrective flush, almost tagging the 200-day moving average of 4091.76, which was stick-saved by a Monday morning post on Truth Social by Donald Trump announcing a pause to his bombing plans of Iranian infrastructure.

The March 23, 2026, intra-day low was 4099.17, for a peak to trough drawdown of -24.33%.

A tag of the 200dma and a breaking of the 20% threshold for a bear market, with a subsequent bounce, presents traders with a conundrum.

Is this a washout and durable rebound or a headline-driven bounce fueled by short covering?

These pages start with the view that gold is in a secular bull market.

Pinebrook got long gold futures back on July 22, 2025. The position was oversized which resulted in a stop-out on August 7, 2025, at a small loss of 1.8% on margin capital.

Position size was recalibrated and another long was established on August 8, 2025. The position was held until October 9, 2025, for a realized gain of 362.33% on margin capital.

The bullish gold thesis was discussed on August 1, 2025.

On September 5, 2026, a long position was initiated on the junior gold miner ETF, GDXJ, which was closed out on October 9, 2025, for a 19.86% return on invested capital.

The note supporting the long miners trade can be found here.

We were admittedly too early to take the other side on October 13, 2025 by going short the junior miners and on October 17, 2025 by going short gold futures.

We got rinsed with a 9.05% loss on the miners and the gold future shorts cost us about half of our gains from the prior gold futures long.

Trading is hard, and when you burn your hand on the stove, you don’t forget that its hot!

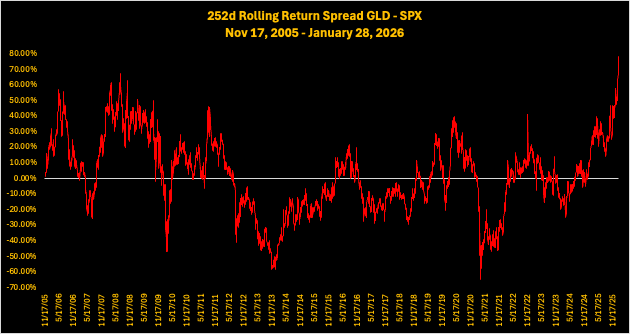

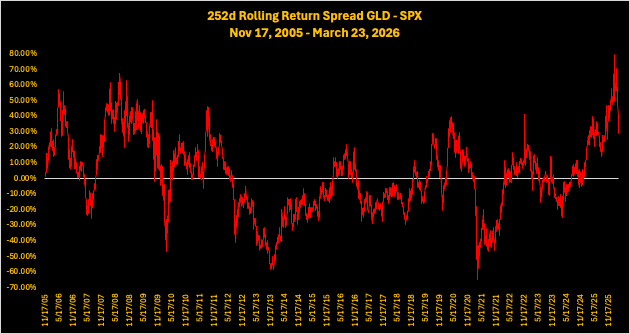

And gold was indeed 🔥, going parabolic as it became 78.81% overbought relative to the S&P500 on a rolling 1-year average going back to November 2005.

This represented 3-standard deviations of overbaughtness relative to the index, which exceeded even the dark days of the global financial crisis at 63.10%.

Crazy doesn’t even begin to describe this chart. 👇

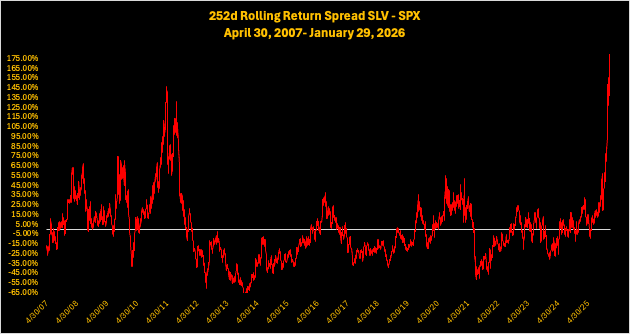

For PNL context, profits were generated from shorting silver via SLV options on January 15, 2026 and then by shorting futures contracts (102% return on margin for one sleeve and a 300.5% return on another) on January 16, 2026 and again on January 27, 2026, which provided the PNL leeway to re-engage gold on the short side.

For new readers, when the SLV ETF peaked on January 29, 2026, it was 261.61% overbought relative to the S&P500, representing over 7-standard deviations! Not a bu-bu-bu-bubble. 🫧

Being risk aware and not forgetting that the gold stove was still 🔥, a short was taken on gold miners on February 2, 2026, by shorting call spreads and purchasing a deep-out-of -the money put option on the GDX and GDXJ ETFs.

All the options expired worthless on March 20, 2026, which generated a profit on the short call spread and a loss on the long put. The net result was a modest profit.

The trade was inefficient due to the high cost of implied volatility in the underlying commodity, which drove volatility in the miners. The return was a pittance compared with what could have been earned by simply shorting the miners or the futures, and sizing correctly for risk management.

The question for these pages now is, is it safe to get back in the pool with the gold sharks?

Let’s unpack this.

We start with updating the GLD-SPX chart listed above.

Despite the corrective pullback, the GLD ETF remains 1-standard deviation overbought relative to the S&P500.

It is cheaper, but not that much cheaper. Charts like this are not predictive. Expensive can get more expensive if le marché deems that to be the path of least resistance.

More buyers than sellers init?

Below is an updated table from a October 20, 2025 note showing post-2006 drawdowns. In addition, the corresponding drawdowns are shown for the two dominant gold miner ETFs, GDX and GDXJ.

So far, this correction is very mid and unexciting.

One could make the argument that the current correction of biggest bull market of this generation is bounded by its strength. The risk is the proverbial knife catch.

Once could also make the argument that a run up characterized by 3-standards deviations requires a lot more air to come out of the bubble. The risk is missing out on a counter trend face ripping rally.

These two arguments are both valid and worthless at the same time because we need to solve for distributional outcomes and path dependencies, not averages.

First, we must acknowledge that the counter trend has already happened.

Gold peaked on January 28th.

It made a violent local bottom on February 5th, for a -11.78% correction.

Most of this was made up by March 2nd, for a 11.36% comeback from the corrective low.

As of March 23rd, gold is -17.19% from the counter trend rally peak.

The trend is broken.

Nice charting and technical analysis.

Second, the narrative soup to describe the price action suggests is not going to go away.

The gold market peaked before the war. Markets always look forward and priced in the dollar pop resulting from a geopolitical risk-off. Buy the rumor sell the fact.

Others did not get the memo and fought the tape, until they were disabused of their optimism by an actual invasion and escalation. Recall Pinebrook was short, albeit for a while, painfully so.

Global risk-off and flight to quality will keep the dollar bid until the market front runs a political solution, however perfect or imperfect it may be, provided it gets physical oil flowing again through the Strait of Hormuz.

The risk-off has led to a deleveraging and degrossing of risk assets. When financial conditions tighten, you sell what you can and have made money in to fund margin calls and shore up balance sheets. It’s at this point the stories become worthless.

Rumor has it that Gulf central banks are unloading gold to meet commitments in the absence of oil revenues. Buy the rumor sell the fact.

Given the above, it is fair to assume that the rumor of continued selling during a cash crunch and tightening financial conditions will carry on until a political solution is forged for mutually agreed oil flow to resume.

But we need another tool to map outcomes and dependencies.