Weekly Signal & Noise Filter

We’re Not Keepin It Real on Christmas

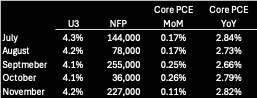

Last week’s FOMC and core PCE releases both came within expectation: a hawkish cut and .11% MoM, respectively. Core PCE came in right on the Pinebrook screws, FTW. This note seeks to explore the nuances in the data and find the signal.

In delivering a hawkish pivot, the FOMC chose the path of least resistance and said the quiet part out loud: it has underperformed on inflation. The main stated reasons, housing and portfolio management services, are a weak basis for taking two cuts out of 2025.

Everyone knows housing is a structural issue with long lags, with an information gap filled in by market-implied rents. Portfolio management services are known to be non-sticky and volatile and are basically a proxy for equity prices. Thus, this is noise.

The FOMC is pricing in the results of the U.S. presidential election and front running the new policy landscape, primarily the impact from tariffs. While Chair Powell was openly transparent about this during his press conference, he had trouble disguising the other motivational factor:

Criticism over the 50-basis point cut in September despite an improvement from the labor market lows of July and a worsening of the inflation trajectory in the same time frame.

While the above may appear to be a surprise, it is a feature and not a bug. In fact, it was a policy choice. The Fed got the outcome it got by prioritizing the labor market over inflation. By Jackson Hole, the Fed deemed the downside risks to the labor market to be greater than the upside inflationary risks. Perhaps they were correct in the counter-factual sense. They were wrong with the results. The hawkish pivot is a regret minimization reaction function without admitting as much.

Beneath the regret minimization attempts belie a more subtle revealed preference. By lowering their 2025 U3 projection from 4.4% to 4.3%, the Fed indicated that they would be less tolerant of unemployment creeping up. This creates a risk that a weak employment report for December (released in January) puts more cuts back on the table.

This is a non-trivial risk as a return to July’s 4.3% level is not a mathematical stretch, given the slow softening of the labor market over the past year.

While the Fed does not make policy off one or two bad prints that go against them, the market prices in and front runs these probabilities. Thus, a weak labor market report at the January release would be met with a fresh repricing of new cut probabilities.

A casual observation would suggest that the Fed has boxed itself in. Less room for margin on the unemployment front, and less room for margin on the inflation front. In short, failing on the dual mandate.

Such an observation would be false. In September, the Fed was giving inflation the benefit of the doubt and focusing on labor market risks. Now the Fed will likely give the labor market the benefit of the doubt as it focuses in on inflation, as even a 4.4% U3 print would put the Sahm indicator at .5, but still below the .56 peak of August. Even a 4.5% U3 print would keep this indicator below the .56 August peak, coming in at .53.

One indicator does not make policy. But it reflects the higher bar for a re-pivot. The Fed will therefore likely tolerate an underwhelming employment report, should one present itself, in favor of more data in February and March.