Weekly Signal & Noise Filter

Stop Obsessing Over U3 – We Will Get There

Jackson Hole has come and gone, and the Powell Fed has pivoted.

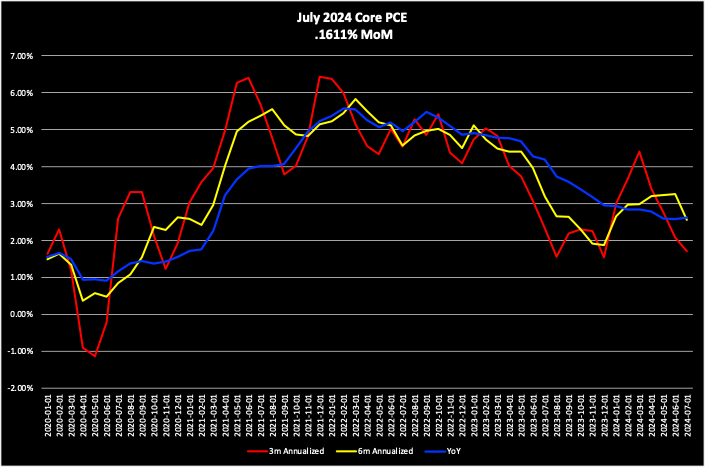

On the surface, Friday’s PCE report was a nothing burger.

Below the surface, the Fed’s preferred inflation gauge of YoY core PCE climbed by 4 basis points, and the 3-month and 6-month annualized rates came in at their lowest levels for this calendar year.

In addition, Pinebrook’s preferred metric, the 6-month annualized rate, registered its first month-over-month decline for this calendar year, decreasing by 69-basis points after rising all year.

In addition, the prior three calendar months (April, May, and June) were revised down by .008, .039, and .062, respectively. Notice the convexity in these numbers, which implies an acceleration in the disinflation trajectory.

At its current trajectory, the inflation measures listed above will experience a slight bump up in the August report (released in September), and then a considerable drop in the September report (released in October) due to base effects.

Base effects are simply measurement echoes of past activity that is making its way through the economy on a forward basis, much as light travelling through space illuminates prior darkness light-years after the fact.

These echoes are the noise. The signal lies in understanding the impact of prior activity on tomorrow’s economy, and ultimately, on the policy reaction function and subsequent downstream impact on asset prices.

The rest of this note is devoted to the above.