Weekly Signal & Noise Filter

The Information Surface Confirms Pinebrook’s Outlook

We have received two meaningful pieces of information, core PCE and GDPNow updates, which confirm Pinebrook’s macro-outlook.

Core PCE

Year-over-year readings declined across all major PCE categories.

OER/shelter remains the pink elephant in the room, accounting for a little more than half of the 75-basis point inflationary overshoot.

Food services and financial services/portfolio management services are two other large categories.

The disinflationary trend stalled in Q1 of this year, and April represented a return to that trend. Despite the stall, progress to the Fed’s preferred inflation gauge of 2% core PCE is on the right track.

Pinebrook expects a material softening in OER/shelter in the May and June reports. The OER/shelter category strength is rooted in the surge in household formation (which itself is a function of the strong labor market) and the resulting home price appreciation episode of 2020-2023. To be clear, home prices are still appreciating, however they are doing so a lower pace.

Should this materialize, the Fed’s 2.6% year-end core PCE target will be hit by this summer. However, that would constitute a head fake. Due to base effects, YoY prints will pick up again in the fall unless there are a series of MoM core PCE prints that come in the low teens or single digits (sub .165% for the detail inclined).

Being at year-end target by the September FOMC meeting will give the Fed the political cover to initiate a cut at that meeting. Any future resulting base effect increases in the YoY measure will be explained away as such, with a lean given to the 3-month and 6-month annualized prints.

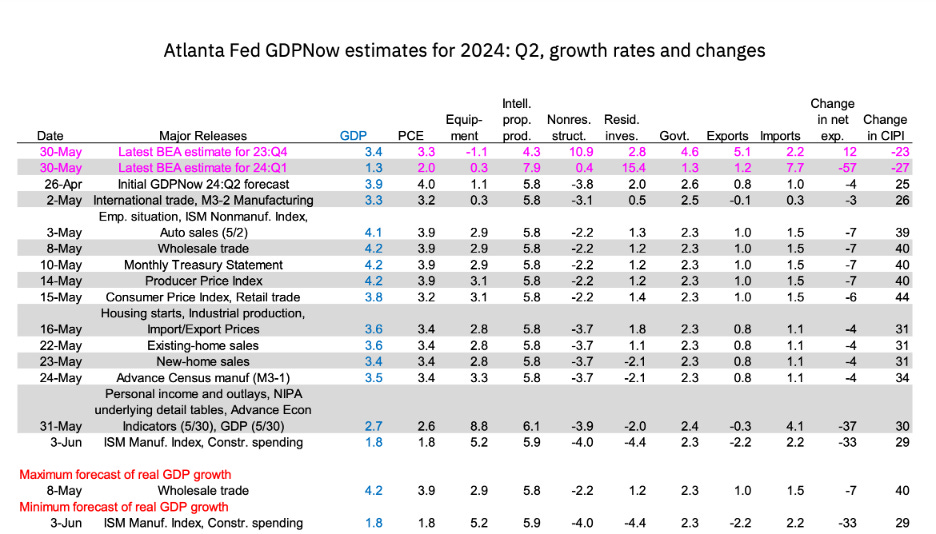

GDP Growth

Since Pinebrook’s U.S. economic update, published April 29, 2024, real growth has steadily been converging to Pinebrook’s non-recessionary slowdown thesis.

After peaking at a 4.2% annualized projection in early May, growth has been downgraded to its current 1.8% expectation. Obvi these projections are fluid, and even sus at the beginning of the quarter, but their precision increases as the we approach the end of the calendar window.

The hurdle to bouncing back to higher levels is now higher as the softer data is baked in the cake.

As anticipated in the April 29 report, the driver has been a pullback in fixed residential investment (FRI). FRI, while a small part of GDP at around 4.5%, has experienced the most volatility compared to any other sector. It has gone from being additive to GDP to being a subtractive of growth.

Bringing it all together, this raises Pinebrook’s confidence for a policy rate cut at the September FOMC meeting.

The market has priced this, and assets reflect all of the above. The question for allocators and traders is, what is next?