Weekly Signal & Noise Filter

Market-Economic Divergence Growing

The core PCE report is the noise, which simply confirmed the continuation of the disinflationary trend that was suggested in the CPI and PPI reports released earlier this month.

The implication is that September remains the appropriate window for a cut in the Fed funds policy rate. This is not new information.

The signal is that if inflation continues to soften at rates consistent with the deceleration that was seen in the May report released last week, then three policy rate cuts will come into play this year.

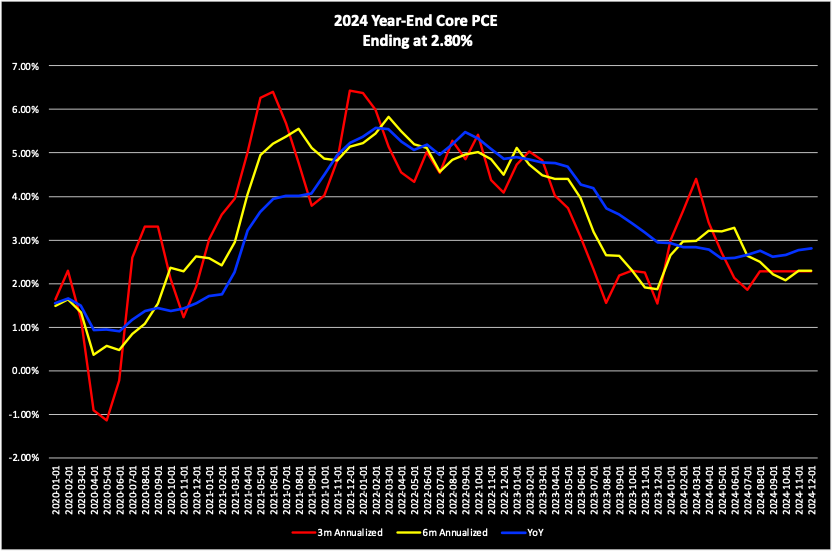

Mathematically speaking, core PCE must average .19% on a month-over-month basis for the remainder of this calendar year for core PCE to hit the Fed’s year-end target of 2.80% YoY.

While the consensus is sus on the above to the point of disbelief, Pinebrook views this as a low hurdle.

Visually speaking, having some iteration of MoM core PCE prints that average .19% and deliver a terminal 2.80% YoY level by year-end looks something like this.

Putting aside that the exact level and sequential distribution of the individual prints is unknowable in advance, ending at 2.8% YoY implies an end to the disinflationary process, if not a minor inflationary acceleration from the current level of 2.57% YoY due to base effects.

The question to ponder then is, is this a reasonable inference given what we know is happening with:

Economic growth (slowing).

The Labor market (wages slowing, U3 rising).

Non-OER prices of goods and services (declining in the aggregate).

OER (starting to slow at a higher rate).

For Pinebrook, the answer is “Hard No”.