Weekly Signal & Noise Filter

Disinflation Remains Intact

The U.S. equity market has been on a one-way directional tear: up in the past 14 out 15 weeks.

This has been in no small part driven by the U.S. treasury market, which has been in a range in the new calendar year after experiencing 2 months of yield compression in November and December of 2023.

The causal drivers of the above are found in the economic data of late 2023, the policy reaction function, and the markets forward looking view of how the economy (and earnings) will evolve in 2024.

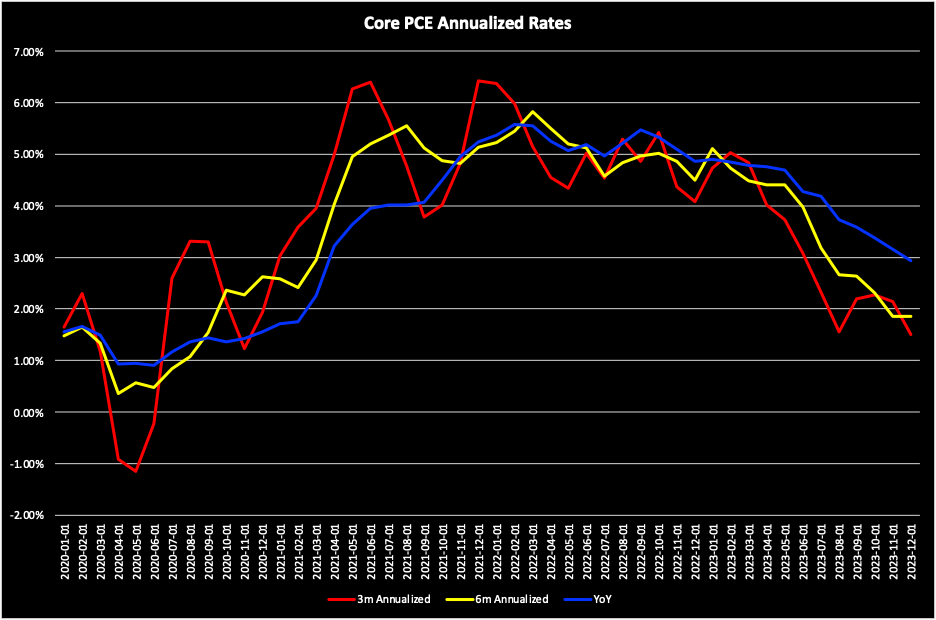

While the disinflationary impulse was in motion before the Fed even started its hiking campaign in March of 2022, the most impactful development of all has been the rate of disinflation experienced since core PCE peaked in 2022, and the collapse in inflation volatility in H2 2023.

Recall, inflation (as measured by the Fed’s preferred measure, YoY core PCE) peaked in February of 2022 at a rate of 5.57%. It then bounced around various 5-handle points before settling at 4.87% in December of 2022.

One can argue that forward looking markets begin to price in the Fed’s abandonment of the transitory approach to setting monetary policy and getting serious about its approach to inflation.

Ultimately this is an academic question of little use for market participants interested in making money.

What matters for participants is that inflation volatility remained elevated in the context of a real economic slowdown in H2 2022.

The combination of heightened recessionary risk along with a more aggressive policy reaction function was feared to be a toxic combination for risk assets as calendar year 2022 ended.

Then the improbable happened.

After an uptick to 4.9% in January 2023, YoY core PCE begin a one-way decent to a two-handle.

The rate of decline accelerated with large downward gaps down in core PCE, especially on a 3-month and 6-month annualized basis in H2 2023.

The disinflationary impulse was more remarkable given an aggressive rate tightening policy by the Fed, ultimately measured in 75bps increments and economic acceleration in H2 2023.

Thus, the decline in the core problem of post Pandemic policy response – inflation – set off a chain of events that soft landed the U.S. economy.

Inflation and inflation volatility collapsed without causing a disturbance to the labor market or economic output.

After its last hike in July 2023, the Fed affirmatively ended its tightening campaign in December 2023 and signaled its intent to commence a rate normalization campaign sometime in 2024.

2024 U.S. corporate profits are expected to deliver their first meaningful growth improvement in two years.

While most fears of an inflationary repeat of that 70’s-show are behind us, inflation will remain a macro thematic driver of outcomes in markets.