Weekly Signal & Noise Filter

The TP Freak Off is Likely Not Over

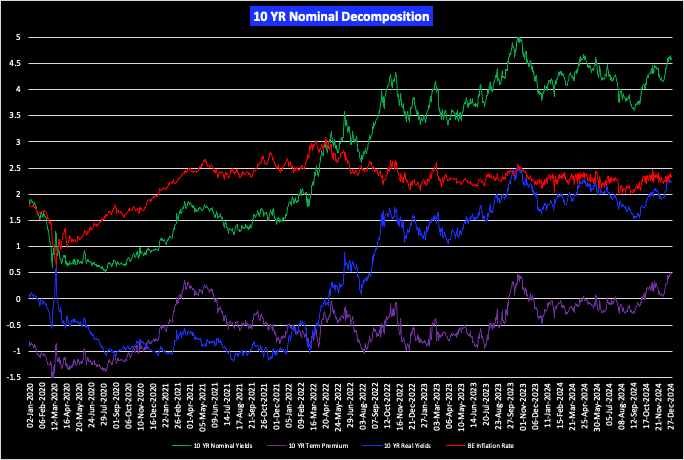

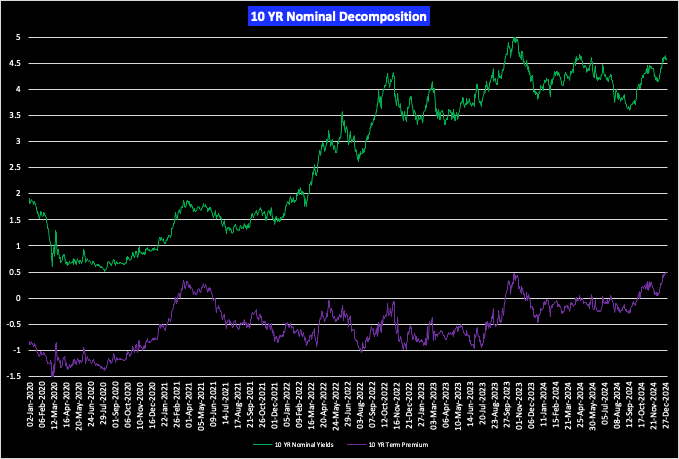

Term premium, not toilet paper.

As discussed in the prior Signal & Noise Filter, price action in 10-year nominal notes is being primarily driven by an expansion in the term premium (“TP”).

There have been two prior notable TP expansions in this cycle that this note will explore and contextualize to see what can be inferred about the current episode. Rest assured, dear reader, this will not be an exercise in technical analysis voodoo applied to Tp’s.

We start with a pretty picture and the data.

The first major episode of TP expansion in this cycle took place between August 4, 2020, and March 19, 2021, from negative 139-basis points to positive 35-basis points, for 174-basis points of expansion in total.

The second TP expansion took place from July 19, 2023, through October 25th, 2023, starting at negative 94-basis points positive and ending at 44-basis points. 138-basis points in total were covered in this TP expansion.

The current episode began on September 11, 2024, and according to the most recent data, is still going as of January 2, 2025. Starting at negative 29-basis points, and currently sitting at positive 49-basis points, for a total of 77-basis points of expansion. The table below summarizes the data.

To the extent the above is of any use, it is simply to point out ranges in TP expansions in this cycle. Thus, this note will not put you, dear reader, through the technical analysis gymnastics of how many days these expansions lasted or their rates of change. That would be as useful as learning that it rained in London last year. What we want to explore are the causal factors, not the events themselves.

Specifically, we want to look at what markets were pricing at the time going forward.

In the first TP expansion episode, markets clearly picked up on the eventual realized rise in inflation. However, inflation did not top out in March of 2021 when TPs made their local peak.

Inflation kept grinding higher for almost another full year after the first TP expansion, with core PCE peaking at 5.57% YoY in February of 2022, and TPs bottoming at negative 65-basis points on April 4, 2022.

It seems paradoxical and contradictory that term premiums would bottom while inflation is peaking. If inflation is kryptonite to bonds, then it would stand to reason that term premiums would be peaking alongside with inflation, and not the other way around.

This however is a cognitive error known as reasoning from a price change, in which a change in price translates into a predictable change in another domain.

Recall that markets look forward, and that markets are extremely good at pricing known, available, information. By the time inflation peaked in February 2022, markets had gotten the memo that the Fed’s average inflation targeting-slash-transitory outlook was shot in the head, and that the Powell Fed was about to get serious about inflation.

The 2022 rise in reals and nominals was mechanically driven by the Fed’s policy rate hiking campaign, not term premiums. Au contraire, term premiums collapsed as markets begin to price in the recession that never came.

Except for a few days in May of 2022, term premiums stayed reliable below zero and went deeply negative as the calendar year progressed irrespective of what inflation was doing.

Term premiums bottomed on December 15, 2022, at negative 97-basis points, reflecting two back-to-back quarters of negative economic growth in H2 2022.

Not surprisingly, the S&P500 bottomed in October 2022, and yield curve inversion as a reliable recession indicator was relegated to the ash heap of history.

The economy came roaring out the gate in 2023. Q1 and Q2 GDP both came in at 2.1%, and Q3 came in at 4.9% and Q4 at 3.4%. These are monster growth numbers and are associated with strong economic recoveries. In addition to growth, core PCE inflation ended 2023 at 3.13% YoY.

Despite mooning growth and collapsing inflation, risk premiums remained deeply negative in 2023, bottoming at negative 93-basis points on July 19, 2023.

Once again, we have another paradox: deeply negative term premiums despite strong growth and a disinflationary process. What exactly were investors so afraid of in the summer of 2023?

Sticking to the principle that markets look forward, term premiums must be contextualized with the potential forward developments at the time.

The potential forward development in question was an accelerating overshoot in the disinflationary process resulting from the most aggressive policy rate tightening campaign in two generations.

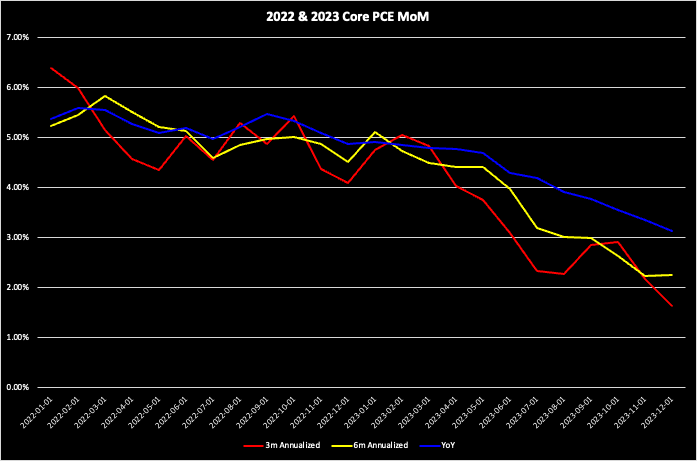

Core PCE peaked in February 2022 and begin a slow disinflationary process thereafter. A year later, the 3-month annualized rate fell apart and was cut in half, going from 5.04% MoM in February 2023 to 2.33% in July 2023 (red line below).

Deeply negative term premiums in July reflected these overshoot fears in the disinflationary process. The July 3m and 6m core PCE annualized numbers of 2.33% and 3.19%, respectively, were already far below the 2023 year-end projection of 3.9% found in the FOMC’s June 2023 SEP.

Markets are the ultimate front running machine, as they were already handicapping what was to come in December: 3m, 6m, and YoY core PCE levels of 1.63%, 2.25%, and 3.13%, respectively.

All below the 2023 year-end projection of 3.7% found in the September 2023 SEP.

Getting back to July 2023, fears of a disinflation overshoot were put aside by a new set of worries on the opposite end of the spectrum.

Q3 GDP was developing into a scorcher, ultimately coming in at 4.9%, as mentioned previously.

August and September core PCE prints came in above expectations, stoking fears of a new round of growth-led inflation (reversed in the October and November prints).

By the time nominals and term premiums peaked on October 25, 2023, markets were looking forward once again. Fortunately, this newsletter was already in the works and there is a documented, written history, to look back on to inform our views today about that not-so-distant past.

October 26, 2023: Pinebrook went long 10s with the idea that the blowout Q3 GDP report had information about future growth slowing due to a high inventory number in Q3 and additional price softening suggesting softening employment cost index measures. Thus, “the idea of a December hike likely gets shot in the head”

November 2, 2023: “A review of the tape brings an observer to the same conclusion.

o Bond yields moved little after the 8:30am release [of the QRA] but really cratered going into the weak ISM, signaling the growth slowdown was going from an academic exercise to an expected one.

o Things really got moving with the release of the Atlanta Fed now-cast that took Q4 GDP down to 1.2% from 2.3% the prior week”.

November 5, 2023: “The Sand Has Shifted” was the note title, and it delivered the following zingers.

o “The first implication is that the Fed hiking cycle is dead in its tracks and is hanging by a thread on life support”.

o “The question now is, when does the easing cycle begin?

November 18, 2023: U.S. Economic Growth Update, “We Have Landed”.

The above is the record, written in real time, detailing the forward evolution of the growth and inflation matrix which the bond market was pricing in, and which ended the second episode of the term premium expansion, returning term premiums to negative 33-basis points on the last trading day of the 2023 calendar year.

As with the second episode of term premium expansion, these pages front ran the summer growth slowdown in 2024. On September 9, 2024, two days before the term premium low of negative 28-basis points on September 11th, a note titled “The Risk Has Gone From a Soft Landing to a Hard Slowdown”.

The note ended by saying, “Thus the Powell Fed will likely be forced to cut more than what is currently priced by markets”.

On September 18, 2024, the FOMC surprised the market with a 50-basis point cut. In doing so, the Fed took recession risk off the table and term premiums began to trend up. The upward trend was fueled by a strong September employment report on October 4th, then again with the election of Donald Trump to the U.S. Presidency.

After yo-yo-ing around the month of November and then almost going negative once again on December 2nd, term premiums are now at their highest level of the post pandemic cycle.

What will send them higher still, or reverse them lower, will once again be contingent on the anticipated evolution of the growth and inflation matrix, which currently being clouded by the uncertainty associated the policies of the new administration.

Tariffs.

Fiscal spending plans.

Regulatory changes.

Immigration/deportation impacts on the economy.

The Fed’s pivot and pickle over a softening labor market and a pause in the disinflationary process.

Feedback loops of the above back into growth, inflation, and the labor market.

Concluding Remarks

Markets look forward to price the good, the bad, and the ugly.

Term premiums falling despite inflation peaking in February 2022 is an example of this.

Thus, term premium expansions and contractions are driven by investor fear and uncertainty of the forward path of the growth and inflation matrix.

These fears are compounded by the uncertainties over the Fed’s reaction function to the above.

Information vacuums generated by outside events, and their unknowable feedback loops, add layers of complexity to the process of price discovery, which amplifies expansions and contractions in term premiums even more.

This analysis makes a lot of sense. I've gained a lot from it. Thank you... Also, are you still holding your 10-year bonds?

What about an incoming treasury secretary who may issue more long term debt?