Weekly Signal & Noise Filter

March 2024 Inflation Projections

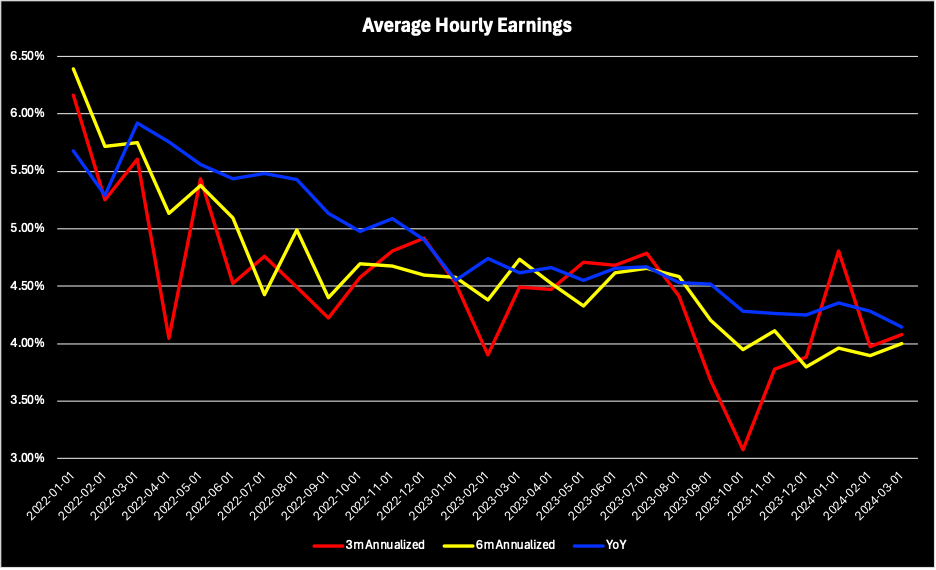

For Pinebrook, the most interesting and relevant part of the employment report was the hourly wage data (AHE).

Both short-term and long-term trends are converging in on the 4% area.

To be clear, this is still above what the Fed considers to be a sustainable, non-inflationary rate of wage growth. On this point, the Fed’s happy place is 100 basis points lower in the 3% area.

Digging deeper, looking at AHE for core non-housing services, where the wage-inflation pass through is strongest, both the short-term and long-term trends are in the 3.5% area.

The continuing strength of the labor market is likely going to lower labor market risks for the Fed. This will be a non-issue if the disinflationary trend continues. The opposite will hold true if inflationary prints come in on the high side.

Pinebrook’s March 2024 inflation projections are the following: