Weekly Signal and Noise Filter

Is the air getting thinner in the rates complex?

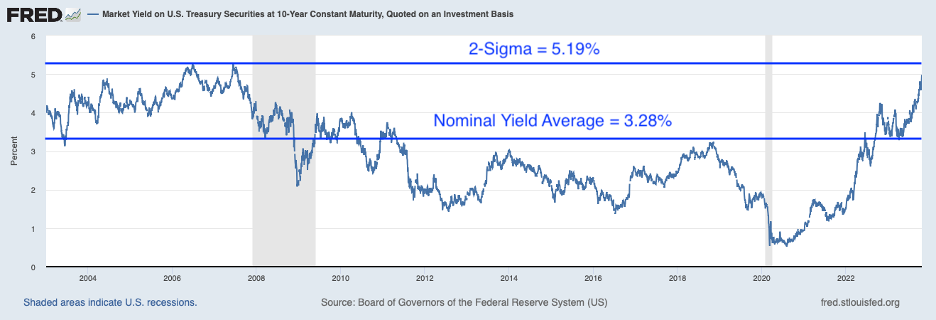

As the 10-year note made new all-time highs last week, briefly tagging above the 5% level intraday, it is fitting that we start this week’s note by asking, how high can we go?

I will be the first to admit that calling tops and bottoms is a tricky business, and there is a graveyard full of callers – top or bottom – with rekt PNL’s.

Still, it is useful to have a reasonable view on where things can go, both within the bounds of “normalcy” (whatever that means) and beyond.

I have focused my work on real rates since summer, which have been on the move after being deeply negative after the start of the pandemic.

As part of a broader thread on Twitter on August 17th, I mentioned that real rates, then at around 2%, could go to somewhere between 2.5% and 3%.

The basis of this comment was a historical review of real rates over the long term.

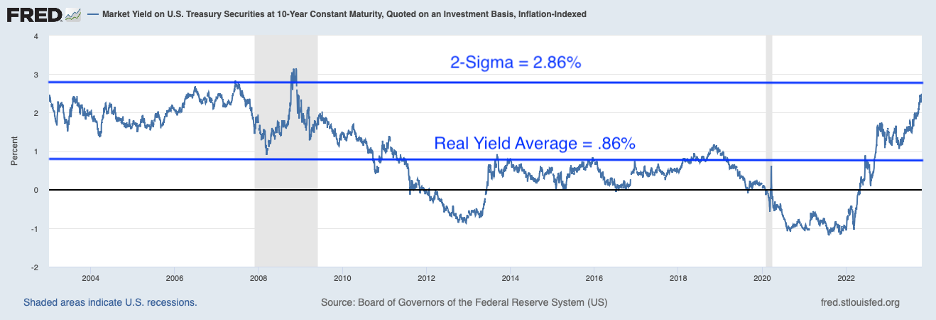

The FRED data sets maintained by the St. Louis Fed go back to January 2003 and reals look like this.

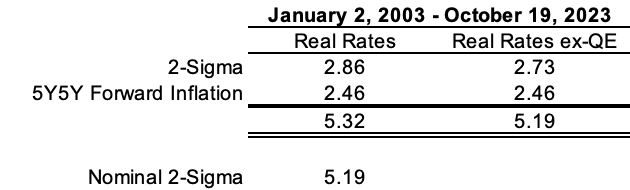

Going back to January 2003, reals averaged .86%, and the 2-standard deviation level is 2.86%.

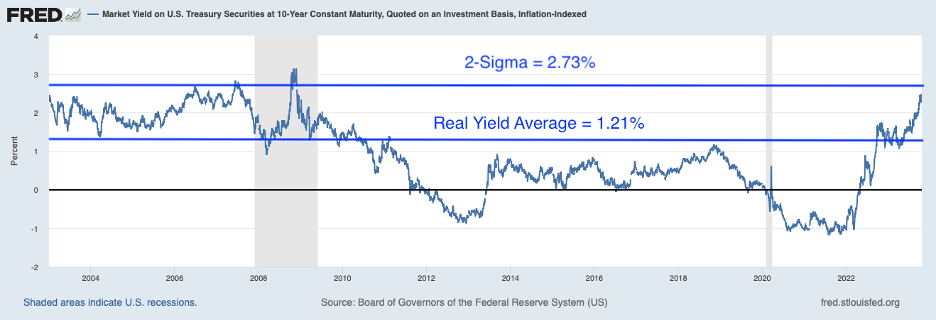

If we strip out all periods with negative real yields due to QE, to get a cleaner look at market pricing of reals, the average rate moves up to 1.21% and the 2-standard deviation level becomes 2.73%.

“Somewhere between 2.5 and 3%” was grounded in this framework, and I think it still applies today.

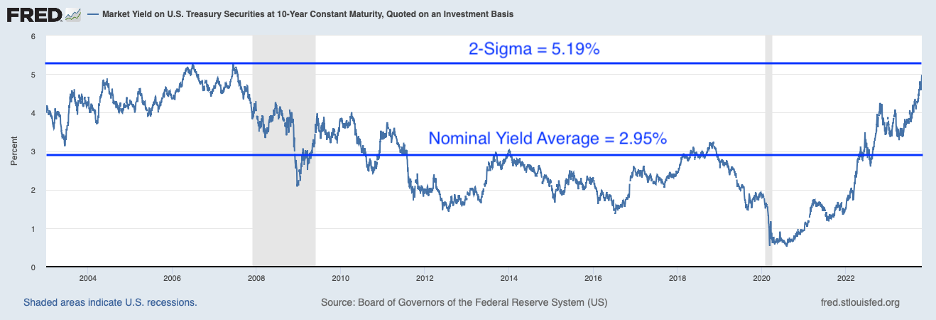

Moving on to nominal rates, which is what most of the world trades, even if to express a view on another part of the rates complex, such term premiums or real rates, gives us this result.

Nominals going back to January 2003 have averaged 2.95%, and have a 2-standard deviation profile of 5.19%.

Repeating the same exercise of adjusting for the QE years, the average nominal yield rises to 3.28% but the 2-standard deviation level of 5.19% remains (changes start at the 3rd decimal place).

If we take the 2-sigma level of real rates and add current inflation expectations as proxied by the 5-year-5-year forward rate (a measure of expected inflation (on average) over the five-year period that begins five years from today), we arrive to nominal levels between 5.19% and 5.32% as an upper bound case in 95% of expected values.

The standard tortured data caveats apply, namely that fat distributional tails do happen, and they happen more often that we think.

The flipside of this is fat tails are not a guarantee.

In any case, this framework provides us with some guideposts for where reals and nominals can top out in the short term.

One final comment on this subject. I am aware and respect the discourse regarding potentially game-changing advances in productivity from AI and GLP-1 anti-obesity drugs that have the potential to raise secular rates.

These advances are years in the making, not something that will be felt in the remainder of this calendar year.

Moving on to Equities

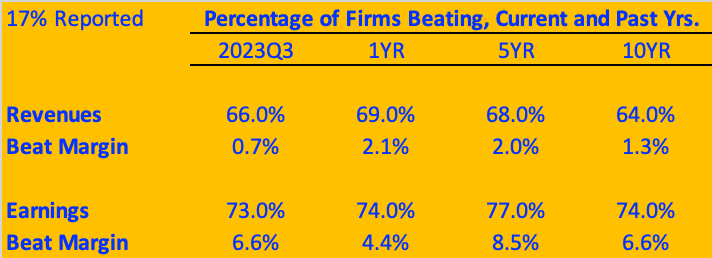

17% of S&P500 firms have reported. Of those firms that have reported, 73% have beat earnings expectations, on average, by a 6.6% margin.

On the revenue side 66% have beat their revenue expectations by a beat margin of .7%.

The following table summarizes the data.

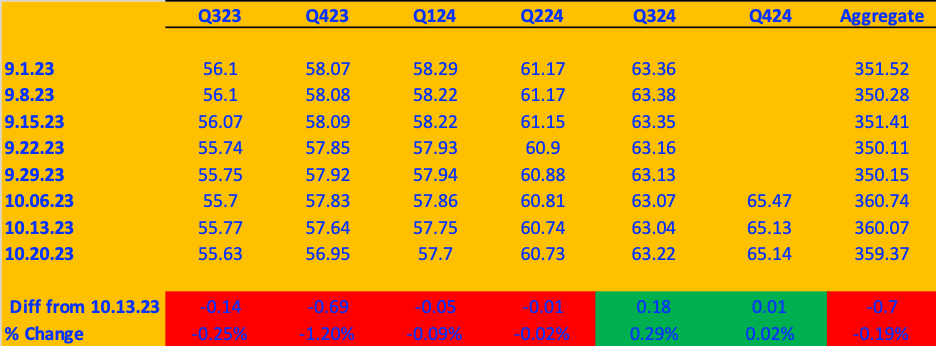

The big egg to crack last week was the Tesla miss. Despite the miss, Q3 earnings hardly budged.

What was telling however, was the drop in aggregate Q4 2023 expectations.

It was the biggest week-over-week drop since I started tracking this data in April of this year.

The next biggest drop for the same quarter was during the week of June 9th, when the WoW drop was -.36%.

A sample of n=1 is statistical noise. Nevertheless, it bears watching as further drops would validate the slower growth in Q4 thesis.

Concluding Remarks:

An upper bound range of 5.19% to 5.32% in the nominal 10-year note is within reasonable bounds of a 20+ year data set.

It is still early days in the Q3 reporting season, but Q4 expectations

need to be watched.

Geopolitical tensions will continue to provide plenty of headline risk to markets.

Thank you for the kind words.

Great piece David. How do you track the earnings data? Is it in Bloomberg somewhere?