Signal & Noise Filter

A New Trilemma

Job’s Day Report.

Geopolitical Shock

Stagflationary supply shock.

These are the three elements of the new Trilemma. The question for investors is, what do they mean and what is the anticipated Fed reaction function to each of them.

We start with the most benign leg of the bar stool, the Friday Job’s Day report.

The February employment report was objectively bad, with the establishment survey delivering a -92K punch to the labor market narrative.

Sprinkle in -69K in downward revisions to December and January, and you have the perfect recipe for a “recession-is-here” cocktail in the financial infotainment space.

This is the noise.

The informational edge is found by looking under the hood and distinguishing between a genuine cyclical turn and a statistical one-off. While the headline figures suggest the labor market got shot in the head, the reality is more likely a combination of methodological “voodonomics” and a weather-driven bullwhip.

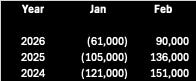

The scale of the swing from January’s strength to February’s weakness is sus. We start with the birth-death model adjustments, which underwent a significant change in 2026.

Geek Note: the birth-death model does not concern itself with organic matters but rather with the opening and shuttering of a business.

The new model adjusted jobs by -61K in January and +90K in February.

Compared to the averages of the prior two years, these adjustments were far more favorable to January and significantly less so for February.

In plain English: the BLS “pulled forward” job growth into January that didn’t actually exist, only to “pay it back” in February.

Birth-death adjustments to Nonfarm Payrolls (NSA)

The effect of this shift is most glaring in private education and healthcare, which have been the main engines of job growth in the past year. If we strip away the seasonal adjustment voodoo, both the “losses” in February and the “gains” in January were relatively small compared to historical norms.

Furthermore, we had a literal labor market disturbance in the form of a Kaiser strike involving 33,000 employees in California and Hawaii. This strike has ended, and a “payback” print can be expected in the next report.

Finally, the weather factor. A relatively balmy January followed by a frigid February created a seasonal whiplash for construction and leisure sectors.

When you combine methodological shifts with cold seasonals, you get a noisy data set that should be faded.

The household survey, which generates the U3 unemployment rate, confirms this.

There was indeed moderate softening. Prime-age employment fell 0.1pp, and the U3 rate rose 12 bps to 4.44% (unrounded).

However, the BLS introduced new population controls that lowered the weighting for prime-aged men and the white population while increasing it for older women and Asians.

The result is the new population controls mechanically lower labor force participation and employment rates but have a de minimis effect on the unemployment rate itself.

The signal is therefore not in the payrolls print, but in the policy-relevant household survey that generates the unemployment rate – which hardly moved.

The above is not sufficient to sway the FOMC and tip the scales of their policy stance.

The pink elephant in the room that is staring at the world is of course the joint U.S. and Israeli military incursion into Iran.

Given the oceans of digital ink that have been spilled on this topic over the past week, what you, dear reader, do not need is another non-expert predictive opinion.

What is needed is a framework for understanding the conflict. For this we turn to Carl von Clausewitz, the Prussian military theorist. In this framework, victory or defeat in war must be judged in the context of the stated political objectives.

In other words, is the use of force moving the needle to the stated political objectives?

The Trump administration has been remarkably consistent in its stated goals – which this writer finds shocking as policy coherence is not a brand fixture of this administration.

The stated goals - reiterated by Rubio, Hegseth, and Chair of the Joint Chiefs of Staff, Dan Caine – are as follows.

Terminate the nuclear weapons program.

Degrade the ballistic missile program and power projection capabilities which target neighboring Gulf states and U.S. military installations in those states.

Degrade the Iranian Navy and secure the Strait of Hormuz for global commerce.

This is not Iraq 2.0: Not a regime change war. There is no humanitarian effort to save anyone. This is not an exercise in nation building or installing a new political system.

Trumps desire for unconditional surrender is not for a sovereign surrender of the Iranian state, but rather for a change of Iranian state behaviors that the U.S. and Isreal are adverse towards.

Collectively, this points to a change in their political business model with respect to their ambitions of being the dominant regional hegemon that calls the shots for everyone else.

Getting back to Von Clausewitz, the question thus is, is the applied force bending Iran towards Trump’s political will? Is Trump getting what he wants?

The nuclear program has not been eliminated. Iran’s uranium stocks have not been affirmatively located, secured, taken into possession, or neutralized/removed. This may require special forces boots on the ground. We are not there yet. ❌

The ballistic missile shield has been seriously degraded and eroded. Missile launch activity is down 90% since open of the war, and drone activity is down 80%. ✅

h/t @ TheStalwart

The Strait of Hormuz remains closed. ❌

In summary: Two out of three objectives not been met. Senior leadership decapitation strikes are multiple layers deep. Iranian control and command of state capacity remains, however weakened. Iran is now in a position where it is reacting to the war, not shaping it.

Iran’s edge is in running the clock on the U.S. and the world even if it gets militarily decimated. Iran’s strategy for winning or surviving is predicated on the view that high energy prices are an intolerable political price for a U.S. President. 🌮🌮🌮

For Pinebrook, the signal is when the Strait of Hormuz is reopened. Everyone needs the oil, including Iran. Everything else is noise.

Now of course markets front run and buy the rumor. The Strait of Hormuz needs not actually be opened. Markets simply need to approximate when this will happen.

In plain English, this means focus on when the oil flows, not on who claims victory.

And what of the stagflationary supply shock?

This is where things get interesting. Unlike political choices and outcomes of military projections of power, understanding a supply shock and the front running the Fed’s most likely reaction function is the domain in which these have pages have something to offer beyond conjecture and guesses.

This analysis will form the basis of the upcoming Market Commentary, in which this framework is used for deploying risk and making money.

Back in the 1970s, when oil prices spiked, the economy went into a tailspin: growth plummeted and inflation skyrocketed (a painful combination known as stagflation).

However, in the 2000s, oil prices rose even more dramatically, yet the economy stayed relatively stable. Why did the same shock (expensive oil) hurt so much less the second time around?

Three key changes in the economy that acted like shock absorbers in the 2000s.

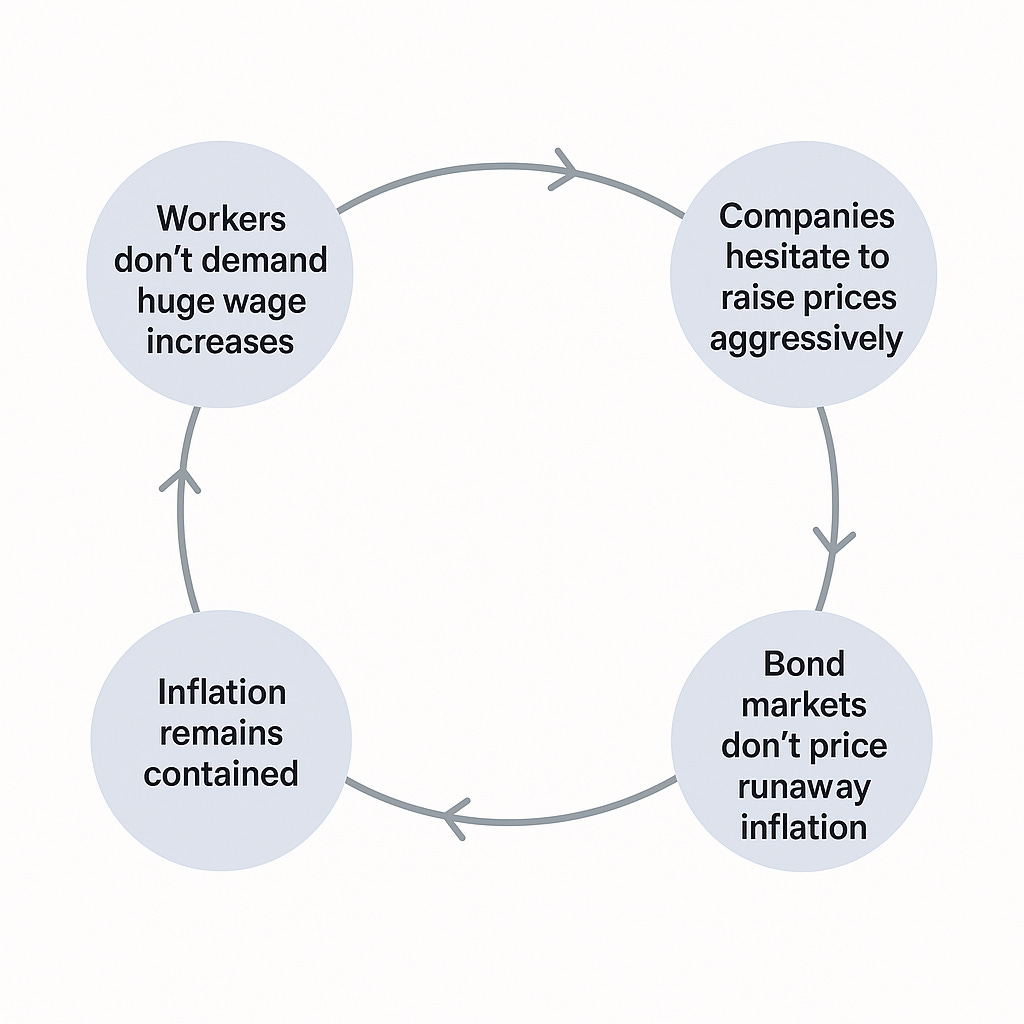

Workers stopped getting automatic raises (wage indexation):

In the ‘70s: Many workers had union-negotiated labor contracts that automatically raised their wages whenever cost-of-living (inflation) went up. When oil got expensive, prices rose, which triggered wage hikes, which forced businesses to raise prices even more—creating a “wage-price spiral.”

In the 2000s: This automatic link mostly disappeared. Because wages didn’t jump immediately when oil prices rose, the spiral never started, and inflation stayed under control.

The Federal Reserve became more credible:

In the ‘70s: People didn’t really trust the central bank to keep inflation down. When oil prices rose, everyone expected high inflation, so they raised their own prices and demands accordingly.

In the 2000’s: The Fed had established a reputation for prioritizing inflation over the labor market. Because people believed the Fed would keep things stable, they didn’t panic or hike prices pre-emptively. This anchoring of expectations kept the economy calm.

We use less oil to produce things:

Modern economies are more efficient. We simply don’t need as many barrels of oil to produce $1 of GDP as we did 50 years ago.

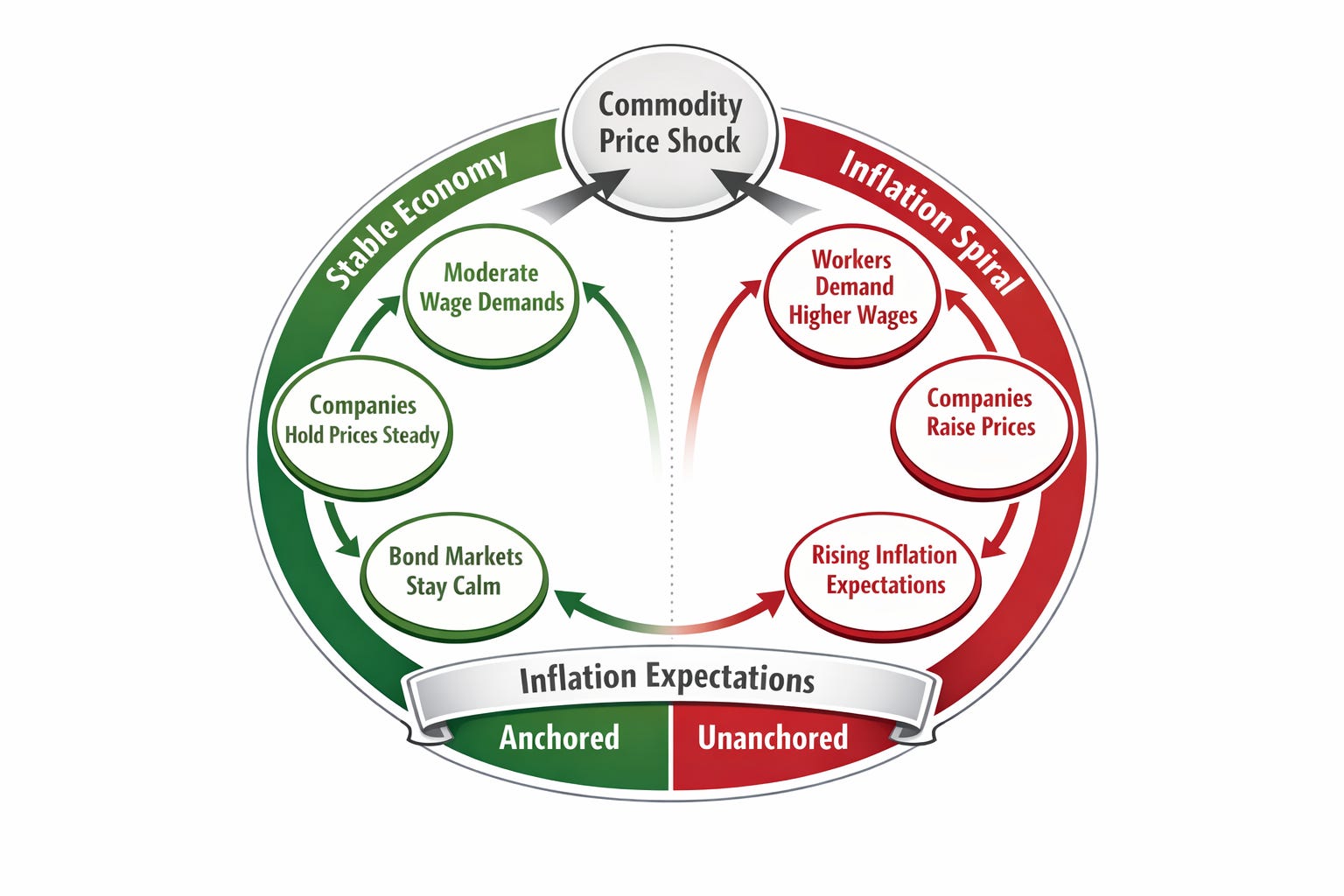

In sum, we can model the changes in this way.

1970’s: Oil shock → inflation → wage increases → more inflation → recession.

2000’s: Oil shock → temporary price increase → limited macro effect.

Oil price spikes used to trigger inflation spirals and recessions, but changes in wage-setting and stronger central bank credibility have made modern economies much more resilient to energy shocks.

What this means is that inflation regimes matter more than oil prices. The economy shifted from a cost-push inflation regime in the 1970s to an inflation-expectations management regime today.

What moves markets now is not the shock itself, but how expectations react. This is why dips get bought.

The Fed’s credibility is the real anchor. After the inflation collapse in the early 1980s, markets bet that if inflation went up, the Fed would crush it. That belief changed behavior everywhere, with a recursive positive feedback loop that looks like this.

Due to the above dynamic, we are still in the green zone below and will likely avoid the red zone.

While the shiny toy model above has its appeal, it must still be squared with the Covid-19 pandemic inflation episode and the post pandemic inflation hangover so that we may contextualize the probability of a repeat.

The vanishing wage spiral mostly held up

COVID supply disruptions + energy spikes (oil, natural gas) → first-round price shocks.

Pent-up demand + fiscal stimulus → extra demand pressure.

Wages started to rise, particularly in services.

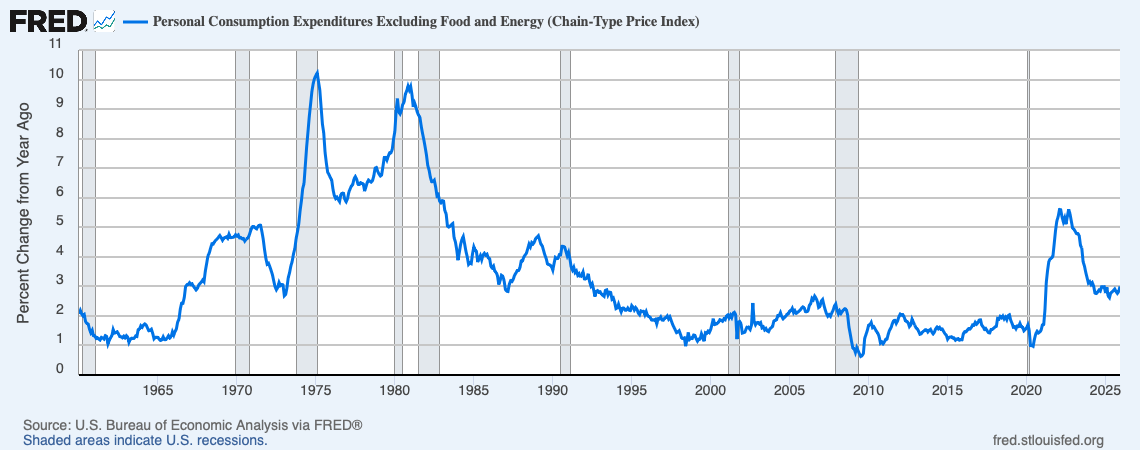

Inflation expectations initially remained anchored, but market pricing (e.g., TIPS break-evens) showed a gradual unanchoring in late 2021/2022.

For the first time in decades, the Fed’s institutional credibility as an inflation fighter came into question because they had waited a long time to raise interest rates, believing inflation was “transitory”.

Thus U.S. inflation break-evens reached a cyclical peak and core PCE hit levels not seen since the early 1980’s.

Once this happened, the Fed came out swinging with the largest and fastest hike cycle in two generations.

Getting back to the shiny toy model and the pandemic experience, the 2021 inflation was much more complex than that of the 1970’s.

The plumbing of global trade broke (port backups, chip shortages), creating sectoral shocks that oil efficiency couldn’t protect us from.

People stopped buying services (travel, gym memberships) and bought stuff (pelotons, home offices). This concentrated demand in one area of the economy, causing prices to spike in a way a general oil shock doesn’t.

This flipped the other way to services after the re-opening of the economy, with a similar price spike unrelated to oil.

Services inflation and low-wage labor markets were key channels.

Fiscal Stimulus, in two words: Gargantuan and inflationary.

The salient economic question for 2026 is not whether there is an oil-induced inflationary price spike. That is a foregone conclusion.

The question is do we have a partial reactivation of the wage-price dynamics with adjacent second-order effects like in 2021, which prolong the current inflation.

In order words, will the post pandemic experience repeat itself?