Sectoral Study - Personal Lenders

A collaboration with Mo, @PersianMacroGuy on X, (formerly Twitter)

Introduction: This is my first collaboration, as well as my first Sectoral Study. The Sectoral Study series is a new line of publishing on this Substack, and one that I hope to do a few times a quarter, either alone in or collaboration with a subject matter expert.

The idea of the Sectoral Study series is to leverage the macro insights of these pages and express them opportunistically in sectors of the market that stand to benefit from anticipated macro developments.

The usual caveats apply, mainly:

1. This is NOT INVESTMENT ADVICE.

This discussion is for informational or educational purposes only, and does not advocate for any particular trade or investment.

Consult your financial advisor before making any trading or investment decisions.

Publication of this content does not constitute an endorsement of any sort.

The business of lending to borrowers was forever changed by, and after, the Global Financial Crisis. The GFC was a Big Bang moment for finance, resulting in a “never again” ethos of regulation that aimed to reign in the excesses of financial capitalism that contributed to the Crisis.

We don’t need to go down the rabbit hole of the alphabet soup of regulations that have put limits on bank balance sheets, leverage, and credit risk. We can simply take it as a given that banks have been neutered from being taxpayer-backed, risk taking hedge funds in drag and converted into public utilities designed to meet the boring public good of intermediating credit to worthy borrowers.

Like water running down a mountain, money flows to where it least resisted. Nor does it ever sleep, as suggested by the awful follow-up sequel to the original classic movie, Wall Street. Thus, private credit, farther from the regulatory arm that governs government-backed lending and banking, is in a secular bull market.

Private Credit

Private credit (“PC”) typically refers to loans provided by specialized investment funds, rather than traditional deposit-taking banks.

PC has grown rapidly over the past two decades. AUM has grown from $200 million in the early 2000’s to roughly $200 billion by the end of 2009, to over $2.5 trillion today. Compare this growth to the high yield bond market, which is roughly the same size as it was in 2014.

PC has also changed the composition of the high yield bond market. The share of BB credits, the highest in the index, has gone from 41% to 51%. The riskier, lower tiered credits have migrated to the PC market.

According to McKinsey, the size of the addressable PC market could be more than $30 trillion in the U.S. alone.

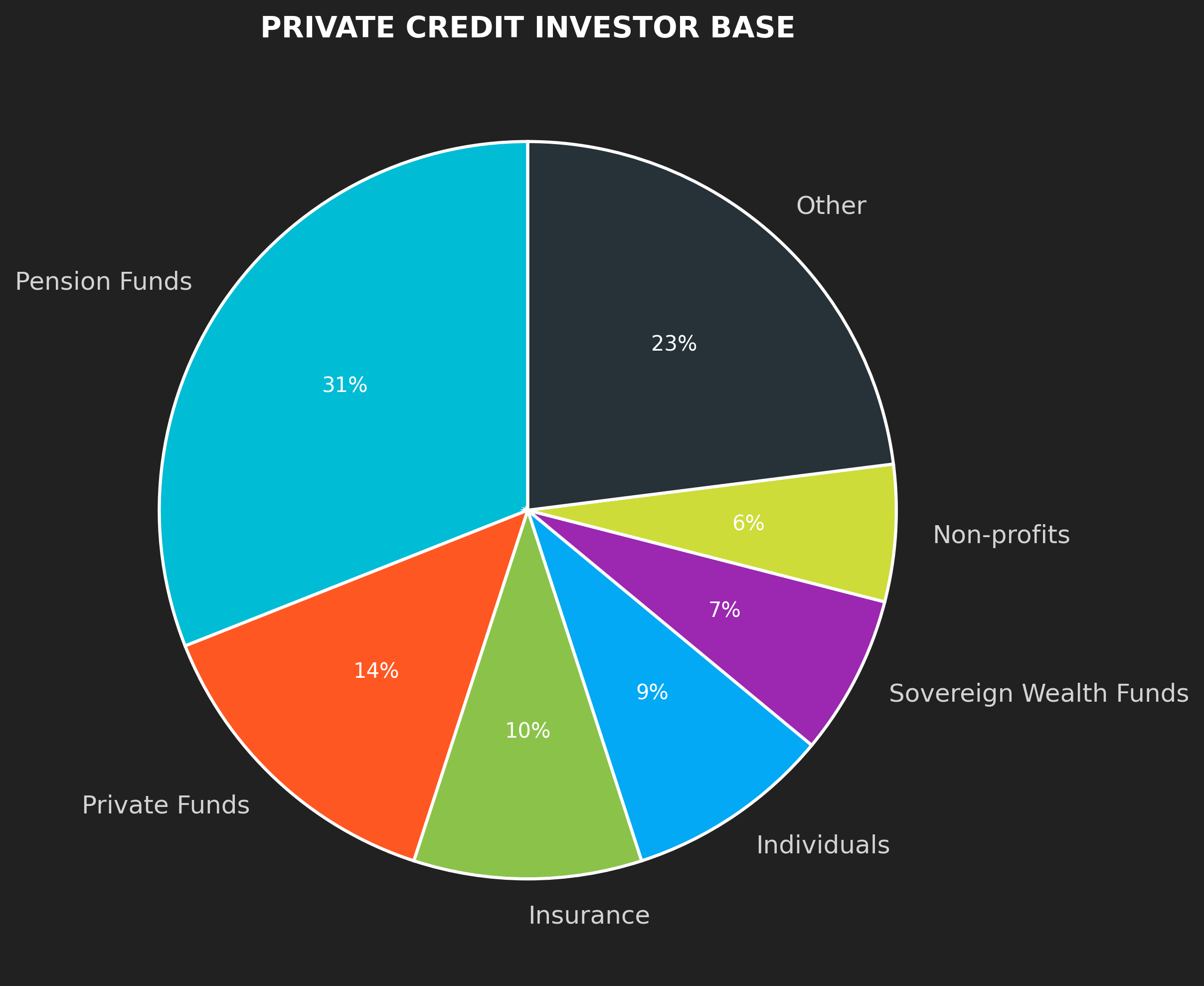

The primary sources of capital for private credit funds are institutional investors that have long-term investment horizons and minimal liquidity requirements. These investors include public and private pension funds, insurance companies, and sovereign wealth funds.

Companies that borrow from private credit funds are typically attracted by the flexibility these lenders offer, especially when compared to traditional banks. Private credit funds often serve firms that banks may overlook, such as smaller businesses or those with high leverage and limited tangible collateral.

These borrowers particularly value how private credit deals can be customized to fit their unique requirements.

The Market for Unsecured Personal Loans

A personal loan is a type of loan that individuals can borrow from a bank, credit union, or other financial institution that can be used for any purpose. It is usually an unsecured loan not backed by collateral such as a house or a car.

Before the Global Financial Crisis (GFC), both home equity lines of credit (HELOCs) and traditional home equity loans were widely regarded as one of the most popular and prudent means through which consumers could address larger temporary credit needs.

The GFC, however, fundamentally reshaped the credit landscape, precipitating a marked decline in HELOC usage and paving the way for the rapid emergence of unsecured consumer debt as a distinct asset class.

This transition is particularly notable given the persistently low-interest rate environment of the post-GFC era, which theoretically should have supported continued strength in secured borrowing. Several factors contributed to this structural shift.

● Heightened regulatory scrutiny and the implementation of the Dodd-Frank Act reduced incentives to offer HELOCs.

● Additionally, banks strategically pivoted toward higher-margin unsecured products, notably credit cards.

● For the consumers, the convenience and immediacy of unsecured lending products grew increasingly attractive compared to the traditionally cumbersome and lengthy HELOC application processes.

Furthermore, advancements in technology, particularly the integration of machine learning algorithms for income verification, fraud detection, and assessing credit worthiness, enabled significant innovation within the unsecured personal loan market. These technological breakthroughs substantially reduced lending risks, streamlined borrower verification, and enhanced user experience, thereby accelerating the growth and appeal of unsecured consumer credit products.

Since the Global Financial Crisis (GFC) of 2008, personal loans have emerged as one of the fastest-growing segments in consumer credit growing at over 10%+ CAGR, faster than credit cards.

There are $251 billion in personal loans (marketplace lending, or “MPL”)outstanding as of Q4 2024, borrowed by 24.5 million borrowers, according to Lending Tree.

● The average balance is $10,244 per borrower, at an average interest rate of 12.26%, and the delinquency rate (60-days or more) is 3.57%.

● Personal consumer loans make up about 1.4% of consumer debt. For comparison, Americans owe $1.211 trillion in credit card debt.

● Personal loans are primarily used to consolidate or refinance credit card debt.

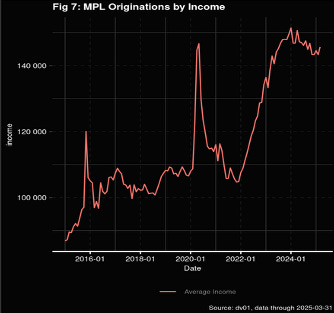

● Average credit score of borrowers in recent vintages is above 730 and the average income above $140k.

Despite experiencing rapid growth since the GFC, the equities of firms in the business of making unsecured consumer loans have generally underperformed as a rewarding long-term investment. The market has become crowded, characterized by intense competition among various providers offering largely commoditized products.

● Traditional credit card issuers such as Discover and Capital One, along with neobanks, fintech startups, shadow banks, and even established investment banks like Goldman Sachs through its Marcus platform, have all entered this competitive market.

● Additionally, the industry has undergone multiple boom-and-bust cycles, reflecting ongoing volatility and challenges inherent to its maturing phase.

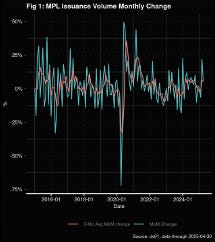

The outbreak of the pandemic in March 2020 compelled FinTech lenders to significantly adjust their operations and tighten lending standards.

As credit markets stabilized and substantial government stimulus flowed into the economy, unsecured personal lending rebounded swiftly, surpassing pre-pandemic origination levels by the end of 2021.

Some FinTech lenders subsequently broadened their credit criteria too aggressively, extrapolating the favorable stimulus-driven conditions indefinitely into the future. This optimism initially spurred dramatic stock price increases for many companies. Notably, Upstart’s stock soared, increasing tenfold in less than a year.

However, the party did not last too long. In 2022, persistent inflation and diminishing fiscal stimulus support led to decreased real incomes and depleted savings for many borrowers. This financial pressure, combined with rising borrowing costs due to the interest rate hikes beginning in March 2022, contributed significantly to escalating delinquencies. By the latter half of 2022, serious delinquency rates surpassed pre-pandemic levels, reaching highs not seen since 2014.

As delinquencies mounted, lenders tightened credit standards. Yet, the most significant blow to loan origination came not from tighter credit alone but from yield lag.

Personal loans are primarily used to refinance existing credit card balances, and credit card interest rates typically lag Federal Reserve rate increases. Personal loan rates lag credit card rates. As funding costs surged, particularly affecting private credit and fixed-income investors, fintech lending platforms effectively froze.

Conditions worsened dramatically with the collapse of Silicon Valley Bank (SVB) and Signature Bank, triggering widespread instability among regional banks. Institutions previously accumulating personal loan portfolios rapidly withdrew from the market, offloading loans aggressively amid heightened regulatory scrutiny.

Many prominent market participants exited entirely. Marcus by Goldman Sachs ceased operations, liquidating their personal loan portfolio and further saturating an already distressed market. At a time when consumer credit card balances hit record highs and credit card rates reached unprecedented levels, consumers found themselves unable to refinance their increasingly expensive debt.

Delinquencies began to recede in 2024, despite upticks in the unemployment rate, as tighter credit conditions and improving economic growth translated into better credit outcomes.

This brings us to today: impairments have returned to pre-COVID levels and, for several consecutive months, have consistently outperformed seasonal trends.