Market Commentary

The EM Trade

This note is a follow up to the last Market Commentary, which indicated a preference for an EM short, as part of the lean towards U.S. assets versus RoW ones.

In making the case for the above, the prior note referenced:

The return of U.S. exceptionalism theme.

A dollar that has stopped falling.

A mean reversion tail event which temporarily favored RoW assets but is now fading and shifting to the historical long-term relationship of U.S. assets > Row assets.

High correlations between U.S. and RoW assets.

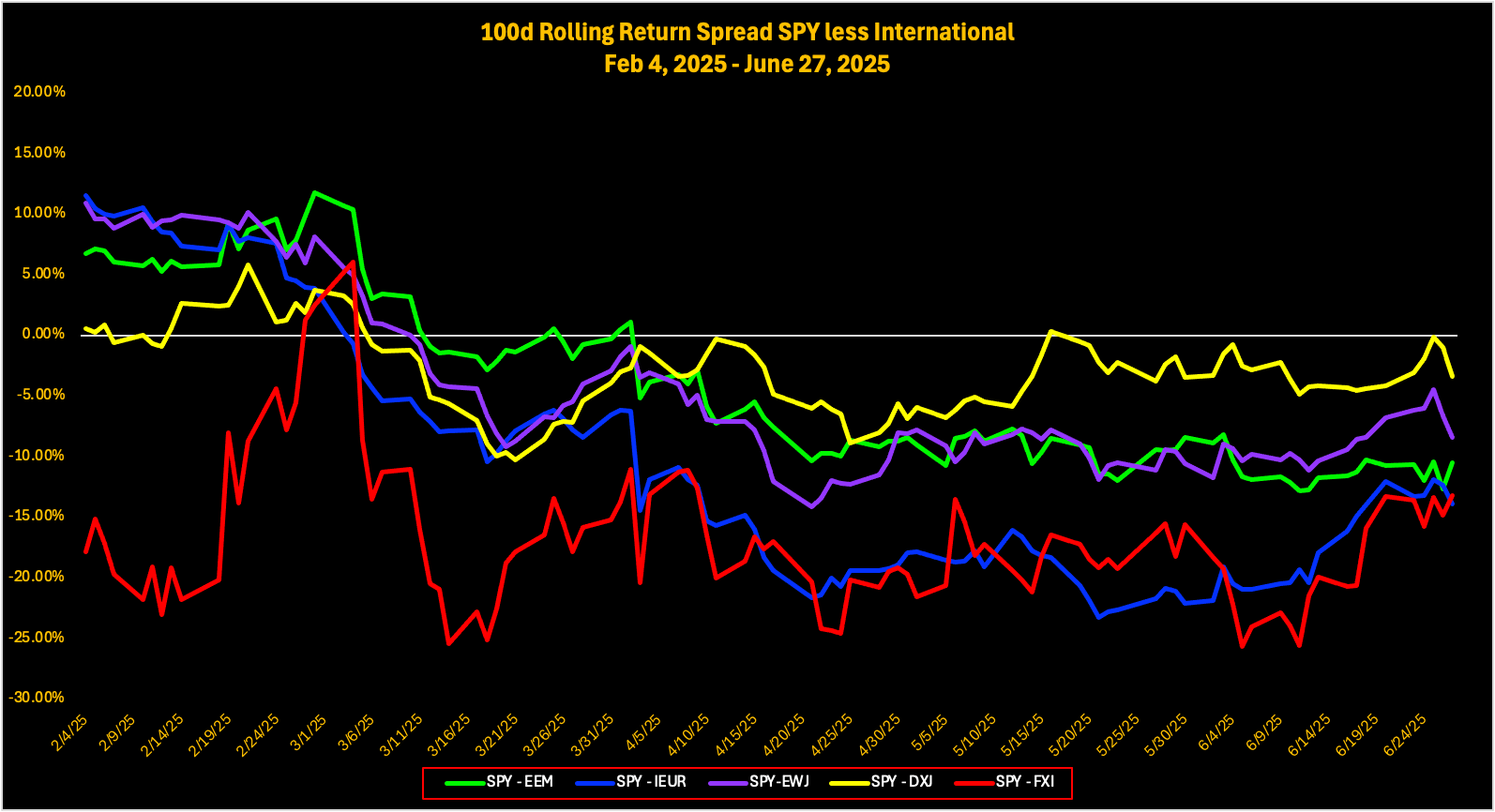

The next observation is that emerging markets are the only non-U.S., RoW asset class that has improvedits performance to U.S. assets since April 23, 2025. Below is a 100-day rolling return chart.

As can be seen, the green line representing the rolling 100-day performance spread between SPY and the EEM ETFs is the only line that has been trending down (if only slightly), going from 9.75% outperformance on April 23rd to 10.53% on June 27th, in favor of EEM vs. SPY.

Below is a table that shows the absolute price performance spread between U.S. assets and RoW world peers. Again, emerging markets are the only asset class that have narrowed the U.S. outperformance spread.

That is, U.S. assets are still outperforming, but less so versus emerging markets.

U.S. assets have consistently increased their outperformance spread over non-EM RoW assets.

In Pinebrook’s view, global investors are going farther out the risk curve for non-U.S. assets, holding on to a fading non-U.S. asset outperformance impulse.

The mean reversion is more pronounced when compared to U.S. big tech, where not even EM has been able to keep up.

As stated on the X social media platform,

Pinebrook is already short FXI, the China ETF. China is 31% of the MSCI Emerging Market index.

Pinebrook is also short ACWX, a global all-country, ex-U.S., ETF. ACWX is weighted approximately 22% towards emerging markets.

Approximately 7.1% of the ACWX ETF is weighted towards China.

Thus, the circle to square is how to efficiently add broad additional EM equity short exposure without duplicating the China exposure.