Market Commentary

Duration is Currently the Most Hated Trade

Yesterday’s 2-yr and 5-yr auctions were deemed sloppy (with a 1-basis point tail), and additional commentary from Minneapolis Fed head Neel Kashkari put pressure on the rest of the rates complex, taking 10-yr yields up by 10 basis points.

Long duration is currently a hated trade, as it should be given:

Spot inflation remains above the Fed’s preferred inflation gauge of 2% YoY core PCE.

The economy and labor market are strong.

An inverted yield curve makes cash more appealing on both a carry and a risk-reward basis.

There is no recession in sight.

Reasonable people can disagree on the semantics of a soft landing. What is beyond dispute is that YoY inflation has been falling (blue line).

Despite the disinflation, duration remains unloved for reasons mentioned above, and in these circumstances, has historically worked best:

In a sudden risk-off crisis.

If recessionary fears start to get priced in. Slowly, then suddenly.

Without the above, we get what we have had since yields bottomed in August of 2020:

The IEF (7-10 year) and TLT (+20 year) treasury ETF proxies are down roughly 25% and 40%, respectively, on a price basis.

These ETFs bottomed in price in October of 2023, but are only up around 5% and 10%, respectively, from those lows.

Buying an asset simply because it is out of favor, hated, or “cheap” (whatever that means) without a pending catalyst is often a disaster waiting to happen. Duration buyers have been taken to the woodshed to catch falling knives and carted out with PNL losses for the privilege.

The post-pandemic inflationary episode presents an anomalous opportunity given the above because the economy is currently experiencing its first disinflationary soft-landing.

Thus, there are two pending catalysts that could change the incentives for buyers to bid duration:

A rapid decline in inflation or inflation expectations (as in H2 2023).

A decline in real rates, which are currently elevated relative to the prior decade.

Let’s have a look at both.

Inflation expectations were higher in the aftermath of the GFC than they are today. The public mood over the bank bailouts and investor hysteria over quantitative easing were contributing factors to elevated inflation expectations.

From 2014 and onward, inflation expectations began a long march down until the covid pandemic and collapsed with the ensuing brief recession (as expectations always do during recessions).

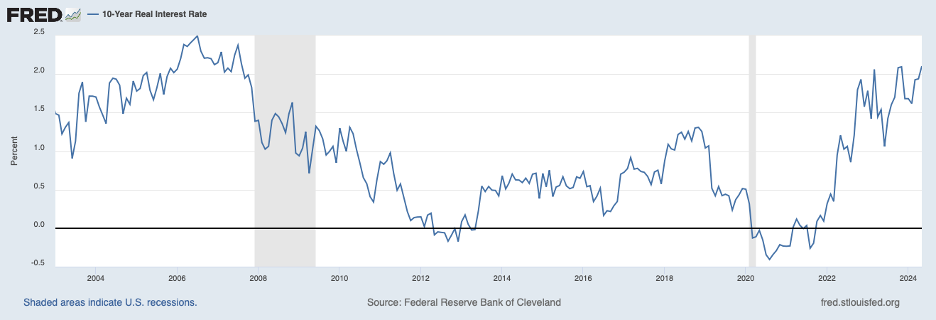

Real Rates tell a similar story.

Reals have not been this high since 2006, at the end of that economic cycle.

Reals are highly correlated to r*, the so-called real natural rate of interest – the level where policy is neither too tight to tip the economy into recession, or too lose to overheat the economy.

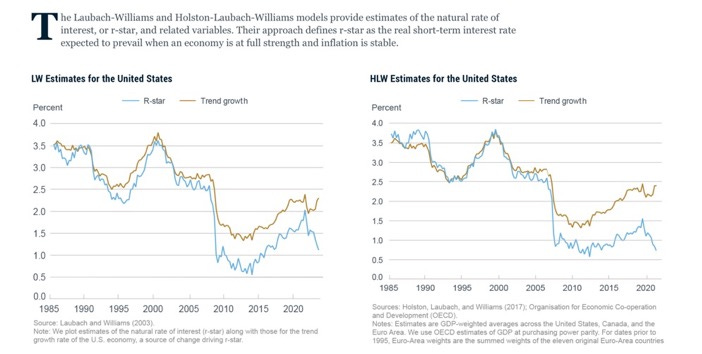

The most current, most state-of-the-art measures of r* show it trending down.

The following except from a note published on March 25, 2024, expounds on some r* math.

“Conjecture aside, we can benchmark current policy to a modified, “Balanced Approach” Taylor Rule favored by Janet Yellen and Ben Bernanke.

Recall, a modified Balanced Approach Taylor Rule overweight’s the coefficient of the output gap, which results in more monetary stimulus to raise the output level up to its full utilization level.

The table below shows a range of policy rates for a given set of inflation and r* assumptions under a modified Balanced Approach Taylor Rule.

Current r* estimates from the New York Fed under the LW and HLW models are at 1.12 and .73, respectively.

Using crude ballpark numbers of inflation of 3% (currently lower) and an r* value of 1.25%, the current policy rate is above the suggested rate of 4.98%.

Even if one considers the very top of the range for projected long-run Fed Funds of 3.8% found in the SEP (which gives an implied r* neutral rate of 1.8%), and 3% inflation, the suggested policy rate is in the 5.5% area.

If inflation hits the Fed’s 2.6% target for calendar 2024, then current rates are indeed restrictive even with a bonkers r* rate that is orders of magnitude larger than the NY Fed’s models above.

Now, the Fed does not make policy according to the shiny toy model or any other interest rate rule.

But the rules and their policy prescriptions allow us to conceptualize and frame the risks of a higher neutral rate.”

In Pinebrook’s view, given the above restrictiveness:

The risks to inflation and the subsequent policy rate lean down.

Real and nominal rates throughout the rate complex are therefore more likely to downshift.

The above is effectively a bet that the market has overestimated the natural rate and is too focused on recent cyclical innovations instead of on the structural developments of the past 21 years.

Concluding Remarks:

Duration is hated asset class and rightfully so.

Being hated or cheap is not a good enough reason for a long, rather an excuse to lose money.

The most obvious catalysts to ignite duration prices are a rapid fall in inflation (expectations), and/or a fall in real rates.

The realization of the above is predicated on a current restrictive policy rate based on a declining r* model framework used by central bank policy making committees.

Going into PCE I would be neutral for now.

Thanks. Very clear. I have a question: Is it a good idea to short TLT right now, or should I take a neutral stance?