March/Q1 2026 Blotter Highlights

Degrossed, but not Fast Enough

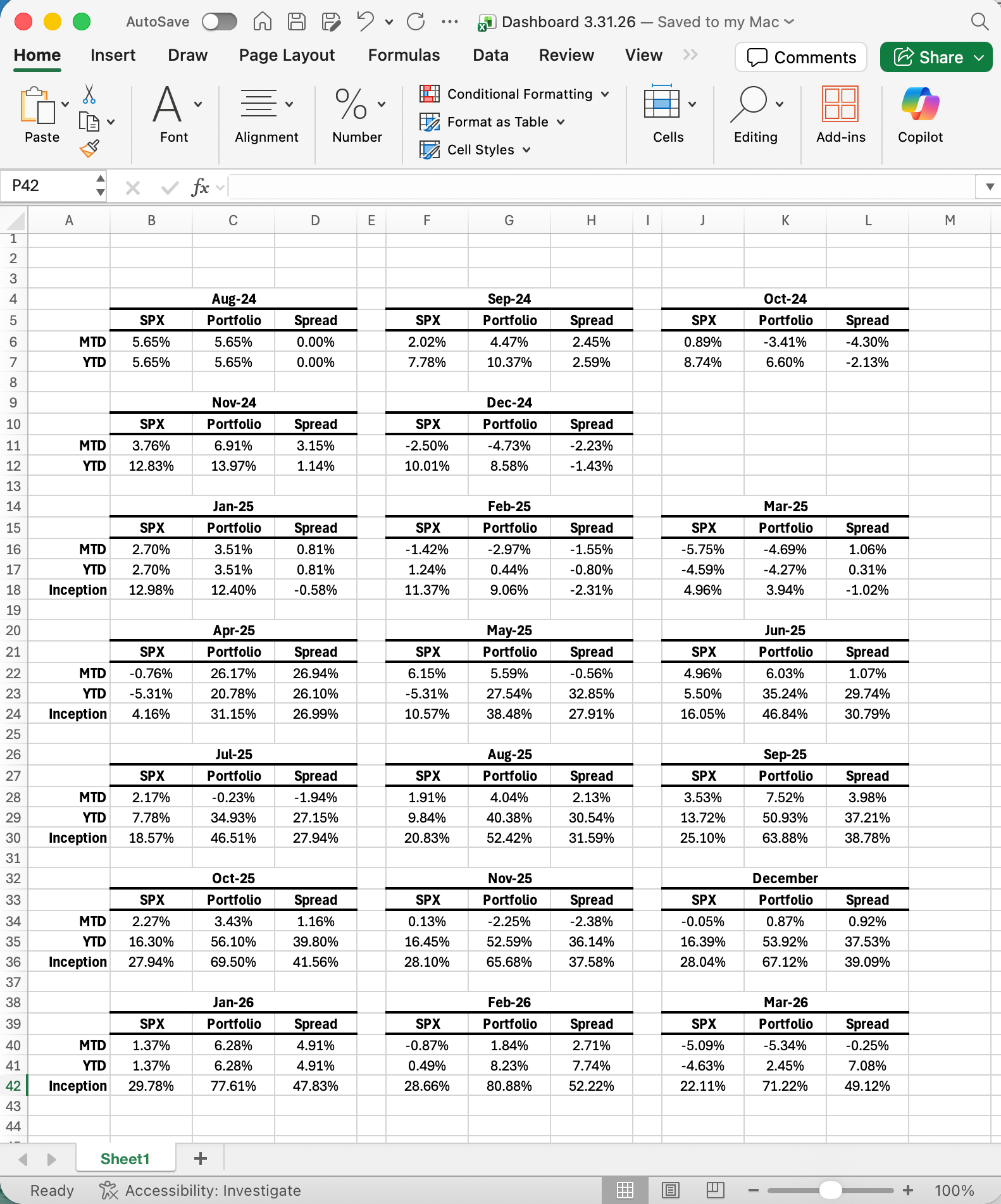

Pinebrook returned -5.34% versus the S&P500 performance of -5.09% for the month of March, resulting in -.25% in monthly underperformance.

For Q1/YTD, the quarter was closed out at 2.45% versus -4.63% for the S&P500, for a positive outperformance of 7.08% in favor of the home team.

The meme of nothing ever happens sent home Mike Tyson’s message, in real time, that everyone has a plan until they get punched in the face.

Pinebrook got punched in the face.

Nothing ever happens refers to the idea that geopolitical headlines, such as the U.S. military buildup in the middle east, is noise with little signal that should be ignored. This noise is amplified by a media-obsessed U.S. president in the form of Donald Trump.

This time proved different, as something did happen in the form of kinetic action and actual bomb dropping in Iran. Then again, there was a 12-day air war with Iran last year.

Wash, rinse, repeat, init?

Le marché certainly priced it as such on Monday, March 2nd. Some undeforming long risk was kicked to the curb (KRE, AIT, WNC, ES-futures) but tragically, long/short pair trades were closed out (EFA/EEM), as well as some short equity hedges (IWM).

The head fake with a punch to the face came on March 3rd, when three core long risk positions in TSM, EWY, and DXJ were torched and subsequently put out to pasture at a loss (but also after large previous gains in the same names).

Seeing the carnage after something did happen, the degrossing of risk started on March 5th, with subsequent liquidations on March 9th, 13th, and the final puke on the 26th.

About 15% AUM was deployed across risk assets that were expected to perform well under an environment of commodity scarcity and supply choke points. While those positions did outperform the broader market, they still resulted in a small loss that contributed -.23% in negative performance attribution to the book.

Fortunately, the short put-spread on gold miners played out and went to zero, which resulted in profits. The expression of the thesis was grossly inefficient however, as the long put also went to zero after having been purchased dearly due to high implied volatility levels. Nevertheless, cash is green and the net PNL contribution was positive at 37-basis points.

On the rates side, we swung for two and got two base hits, having shorted U.S. 10’s (ZN) in early March and then taking the other side of the short end in late March with a long in 2’s (ZT).

Disaggregating the portfolio returns and ranking them by source reveals the following:

2.41% in commodities.

56-basis points from rates.

40-basis points from options.

-92-basis points from equities.

The process of degrossing was too slow, and re-engaging on the short side did not happen due to risk aversion in the context of a headline-driven market that could blow short positions out of the water.

Warren Buffett’s first rule of portfolio management is don’t lose money. His second rule is respecting the first rule.

The month of March was an exercise in frustration of the above.

If the future evolution of the economy is anywhere near what these pages expect, we are in the early days of a massive opportunity set for active management and for taking risk on both the long and the short side.

Volatility will increase and tails will become wider as both sides in the Iran conflict chose to escalate before reaching an off-ramp.

There is money to be made in this sequence of events.