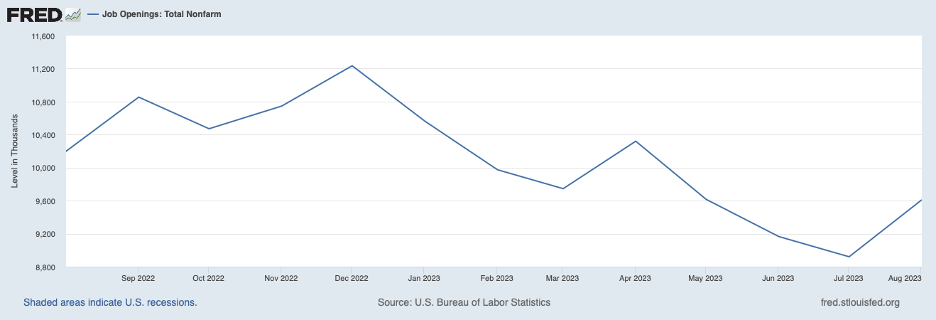

JOLT'd

The JOLTS jaw dropper yesterday got the bond market all excited yesterday, with job openings mooning to 9.6 million.

The theory here is that the labor market has been cooling, and this print threw a wrench into future expectations of labor market softening – prompting the idea that another rate hike in calendar 2023 is live and on the table.

I think that is noise.

First, this data comes with a 1-month delay. I prefer the weekly initial and continuing claims data as an almost real-time read on the labor market.

Second, openings are somewhat sus, as many employers advertise openings just to gauge labor market dynamics such as current salary expectations, without any intentions of hiring anyone.

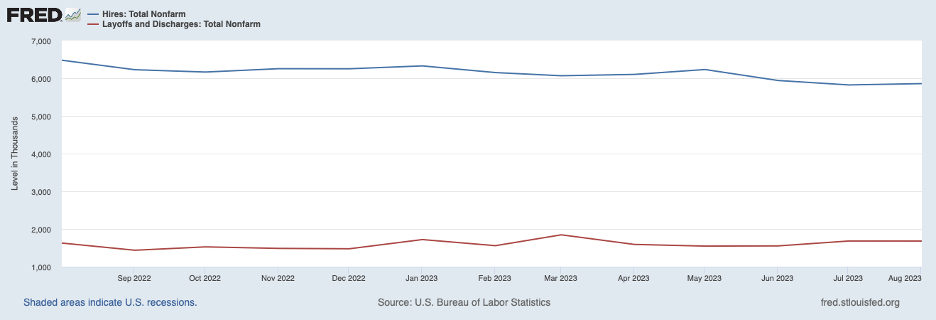

For this reason, I consider openings to be “soft” data. I prefer actual hires, layoffs, and quits. And these numbers were relatively unchanged.

The signal is in what JOLTS may mean for NFP on Friday

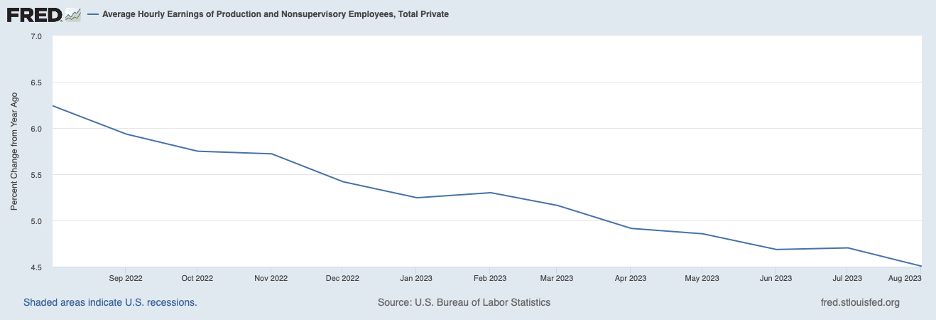

Given the flatness of hires and layoffs, I am expecting wages, as measured by average hourly earnings for production and non-supervisory workers, to continue their downward trend, to maybe 4.4% or 4.3% YoY (currently 4.5% YoY).

This is what I am looking for in Friday’s labor market report because this goes to the heart of the Fed’s policy objectives for the labor market as a transmission mechanism for lowering aggregate demand and sticking the soft landing: less aggregate spending without crashing the labor market.

This would be consistent with my current thesis of a non-recessionary pullback in nominal GDP.

Good luck on Friday!

Hi Tnx.

My DMs on X are open. Feel free to hit me up if you have any questions.

Excellent article!