U.S. High Frequency Data Point

ISM Edition

Service Sector Strength Points to Continued Expansion

The December ISM Services report provided a robust signal this morning, suggesting that the service sector—which comprises approximately 75% of U.S. economic activity—remained resilient and well-distanced from recessionary territory through year-end.

Notably, every primary component of the index moved in a favorable direction.

Key Data Points

The report highlights a broad-based expansion across the service economy:

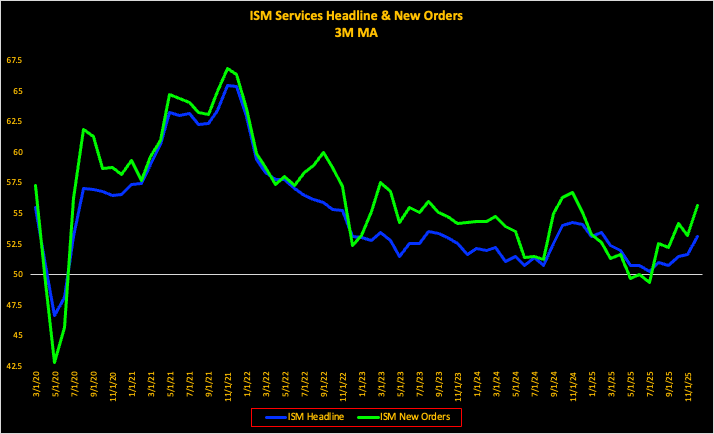

While the ISM manufacturing report on Monday suggests continued contraction in that sector of the economy, the dominant service sector data released today showed a strong inflection up in December, especially in the important and forward-looking new orders component of the index.

Below is a 3-month moving average chart which smooths the data for the services headline index and new orders sub-index.

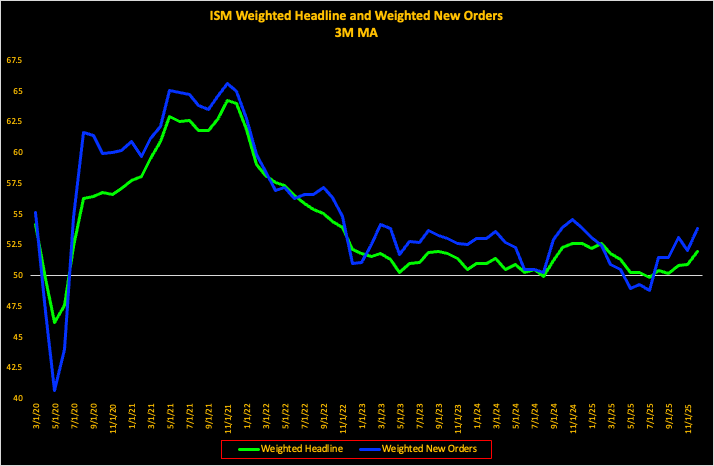

Taking the headline data for both manufacturing and services, along with the new orders indexes for both manufacturing and services and weighting them in proportion to their contribution to GDP output, we have a chart that looks like this.

Even with a lagging manufacturing base, the weighted averages of both headline and the forward-looking new orders subcomponent of both manufacturing and new orders point to a very clear expansion of the economy.

Hold your beer and keep taking risk.

Do you remain fully allocated, or do you see reason personally for increased cash allocation?

Thank you, David!