February ISM

The Growth Impulse Refuses to Fade

The narrative of the U.S. economy remains one of stubborn, aggressive resilience.

The movement of the real economy - specifically the services sector - continues to shout otherwise.

Monday’s ISM Manufacturing report was good, but today’s ISM Services report for February was even better.

Together, they effectively negate the likelihood of an economic downturn in the next several months, provided we can avoid a complete derailment from geopolitical idiocy in the Middle East.

Recall that services represent roughly 75% of all economic activity. While manufacturing has spent the last year in an active restocking cycle, the services sector is now providing the heavy lifting for the broad-based economic floor that has been tracked since January.

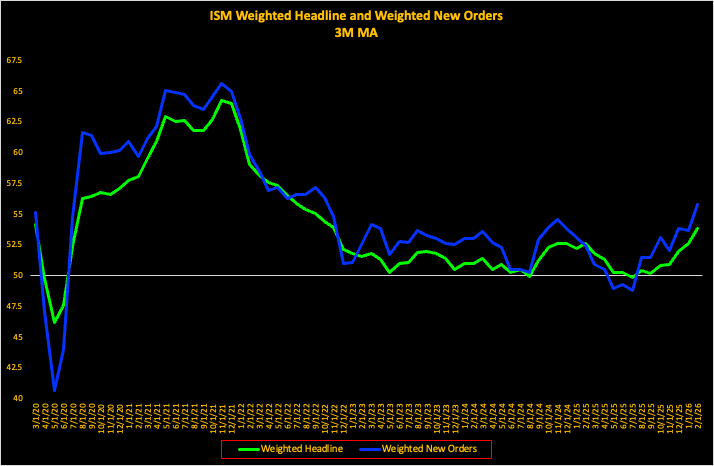

Thus, the Pinebrook approach of weighing manufacturing and services by their respective contribution to the economy provides, and then smoothing the data, provides more signal than a simple spot sample.

This is done below for both headline manu and services, and new orders for manu and services.

Headline Momentum: The services headline number hit 56.1 for February. When weighted with manufacturing, the three-month average is 54.14, which is solidly positive and suggests firms are no longer in a “wait-and-see” mode.

New Orders Surge: This is the breakout. The forward-looking new orders component for services improved to a robust 58.6. The economically weighted three-month average (including manufacturing) hit 55.18 - the highest level in over three years.

The January ISM note laid out a clear restocking cycle thesis. Now, we were moving from restocking to a proactive growth phase.

February’s data hasn’t just confirmed this, it has accelerated it.